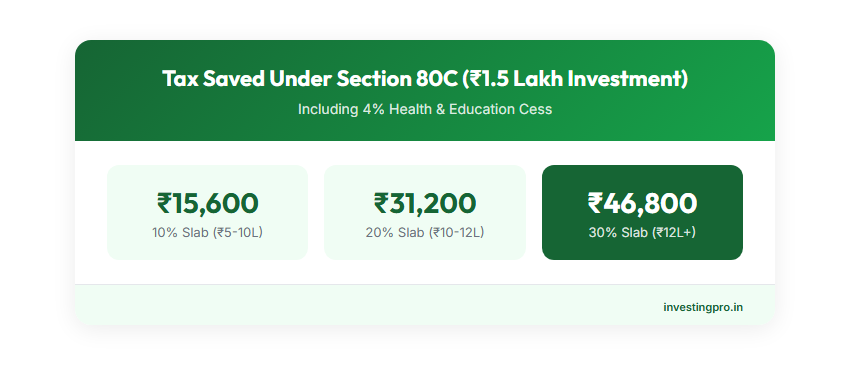

Section 80C of the Income Tax Act 1961 allows Indian taxpayers to claim deductions of up to ₹1,50,000 per financial year from their gross taxable income. This single section covers a wide range of investments and expenses — from ELSS mutual funds and PPF to life insurance premiums and children's tuition fees. For someone in the 30% tax bracket, fully utilizing Section 80C saves ₹46,800 in taxes every year (including 4% cess). This guide covers every 80C option available in FY 2025-26 (AY 2026-27) with real ₹ examples for different salary levels.

Key Takeaways

- Maximum deduction under Section 80C: ₹1,50,000 per financial year (combined limit for all 80C investments)

- Tax savings potential: ₹46,800 (30% slab), ₹31,200 (20% slab), or ₹15,600 (10% slab) — including 4% health and education cess

- 80C is only available under the Old Tax Regime. The New Tax Regime (default from FY 2023-24) does not allow 80C deductions

- ELSS mutual funds offer the shortest lock-in (3 years) among all 80C options with potential for highest returns (12-15% CAGR historically)

- EPF contributions by salaried employees count toward the ₹1.5 lakh limit — check your payslip before investing separately

- Combining Section 80C with 80CCD(1B), 80D, and Section 24(b) can reduce taxable income by over ₹5 lakh for salaried individuals

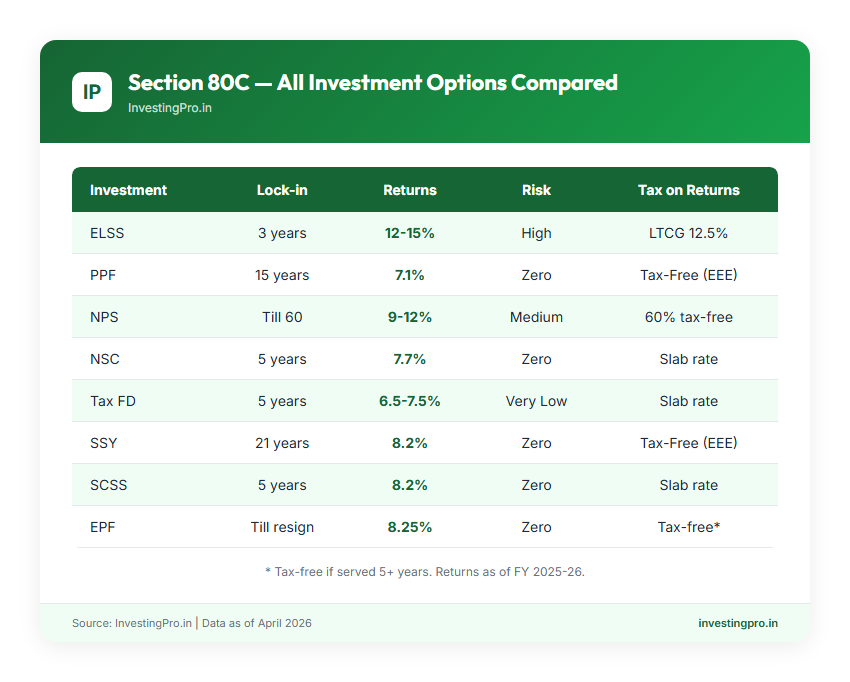

All Section 80C Investment Options — Comparison Table

Before choosing where to invest, here is every instrument that qualifies under Section 80C. Compare them side by side on what matters: lock-in period, expected returns, risk level, and how the returns are taxed.

| Investment | Lock-in Period | Expected Returns | Risk Level | Tax on Returns | Best For |

|---|---|---|---|---|---|

| ELSS Mutual Funds | 3 years | 12-15% (historical) | High (equity) | LTCG above ₹1.25 lakh taxed at 12.5% | Young investors, wealth creation |

| PPF | 15 years | 7.1% (govt. set) | Zero (sovereign) | Fully tax-free (EEE) | Conservative investors, long-term savings |

| NPS (Sec 80CCD(1)) | Till age 60 | 9-12% (equity), 7-9% (debt) | Medium | 60% corpus tax-free on maturity; annuity taxed | Retirement planning, additional ₹50K deduction |

| NSC | 5 years | 7.7% | Zero (sovereign) | Interest taxable (but reinvested interest qualifies as 80C in Year 1-4) | Low-risk investors wanting fixed income |

| Tax-Saving FD | 5 years | 6.5-7.5% | Very Low | Interest fully taxable at slab rate | Senior citizens, risk-averse investors |

| Sukanya Samriddhi (SSY) | 21 years (partial at 18) | 8.2% | Zero (sovereign) | Fully tax-free (EEE) | Parents of girl child (below 10 years) |

| SCSS | 5 years | 8.2% | Zero (sovereign) | Interest taxable at slab rate | Senior citizens (60+) |

| EPF (Employee Share) | Till retirement (5 years for tax-free withdrawal) | 8.25% | Zero (sovereign) | Tax-free if service > 5 years | All salaried employees (auto-deducted) |

| Life Insurance Premium | Policy term (5+ years) | 4-6% (traditional plans) | Low | Maturity tax-free under Sec 10(10D) if premium < 10% of sum assured | Family protection (term insurance recommended) |

| Home Loan Principal | Loan tenure | N/A (expense, not investment) | N/A | N/A | Home buyers with active home loan |

| Tuition Fees | N/A | N/A (expense) | N/A | N/A | Parents paying school/college fees for up to 2 children |

Important: The ₹1.5 lakh limit is a combined limit across all these instruments. You cannot claim ₹1.5 lakh in ELSS and another ₹1.5 lakh in PPF — the total across all 80C investments and expenses must not exceed ₹1,50,000.

Old Tax Regime vs New Tax Regime — Does 80C Still Make Sense?

Since FY 2023-24, the New Tax Regime is the default for all taxpayers. It offers lower slab rates but removes almost all deductions, including Section 80C. You must actively opt for the Old Tax Regime to claim 80C benefits.

So when does 80C make sense? The break-even depends on your salary and total deductions.

| Gross Salary | Tax Under New Regime | Tax Under Old Regime (with 80C + 80D + HRA) | Better Regime |

|---|---|---|---|

| ₹6,00,000 | ₹0 (rebate u/s 87A) | ₹0 | New Regime (simpler) |

| ₹10,00,000 | ₹54,600 | ₹46,800 (with ₹3L deductions) | Old Regime (if you invest) |

| ₹15,00,000 | ₹1,45,600 | ₹1,09,200 (with ₹4.5L deductions) | Old Regime (clear advantage) |

| ₹25,00,000 | ₹3,64,000 | ₹2,80,800 (with ₹6L+ deductions) | Old Regime (significant savings) |

Rule of thumb: If your total deductions (80C + 80D + HRA + Home Loan Interest) exceed ₹3.75 lakh, the Old Tax Regime usually saves you more tax. Use our Tax Calculator or read our Old vs New Tax Regime Guide for a personalized comparison.

Detailed Breakdown of Each 80C Option

1. ELSS Mutual Funds — Our Top Pick

Equity Linked Savings Scheme (ELSS) funds invest primarily in equities and qualify for tax deduction under Section 80C. Among all 80C instruments, ELSS offers the shortest lock-in period of just 3 years and the highest potential for wealth creation.

| Parameter | Details |

|---|---|

| Lock-in Period | 3 years (shortest among all 80C options) |

| Expected Returns | 12-15% CAGR (historical 10-year average) |

| Risk Level | High (equity market risk) |

| Minimum Investment | ₹500 (SIP) / ₹500 (lump sum) |

| Tax on Returns | LTCG above ₹1.25 lakh/year taxed at 12.5% |

| Who It's Best For | Investors aged 25-45 comfortable with equity volatility |

If you invest ₹1,50,000 in ELSS through a monthly SIP of ₹12,500 and earn 12% CAGR, your corpus after 3 years would be approximately ₹5.4 lakh. After the 3-year lock-in, each SIP installment becomes redeemable on its own completion date.

InvestingPro Verdict: ELSS is the best 80C option for anyone with a 5+ year horizon who does not need the money soon. The 3-year lock-in is manageable, and equity returns significantly outpace fixed-income alternatives. Start with a SIP — do not invest a lump sum in March. Read our Best ELSS Funds for 2026 guide for top-rated fund picks.

2. Public Provident Fund (PPF)

PPF is India's most popular tax-saving instrument for conservative investors. It offers guaranteed returns, sovereign safety, and completely tax-free maturity — the only true EEE (Exempt-Exempt-Exempt) product for the general public.

| Parameter | Details |

|---|---|

| Lock-in Period | 15 years (extendable in 5-year blocks) |

| Current Interest Rate | 7.1% per annum (compounded annually, set quarterly by govt.) |

| Risk Level | Zero — backed by Government of India |

| Minimum Investment | ₹500/year (Max: ₹1,50,000/year) |

| Tax on Returns | Fully tax-free — interest, partial withdrawals, and maturity all exempt |

| Who It's Best For | Risk-averse investors, long-term retirement corpus building |

Investing ₹1,50,000 every year in PPF at 7.1% interest yields approximately ₹40.7 lakh after 15 years — entirely tax-free. Partial withdrawals are allowed from the 7th year onwards.

InvestingPro Verdict: PPF is ideal as the debt portion of your 80C portfolio. It is the safest way to grow money tax-free in India. However, the 15-year lock-in means this money is truly locked away. If you are young, pair it with ELSS rather than putting the full ₹1.5 lakh here. Use our PPF Calculator to project your maturity amount.

3. National Pension System (NPS)

NPS serves dual duty under the tax code. Your contribution up to ₹1,50,000 qualifies under Section 80CCD(1) within the 80C limit. Additionally, you can claim an extra ₹50,000 deduction under Section 80CCD(1B) — making NPS the only instrument that offers deductions beyond the ₹1.5 lakh cap.

| Parameter | Details |

|---|---|

| Lock-in Period | Till age 60 (partial withdrawal allowed after 3 years for specific purposes) |

| Expected Returns | 9-12% (aggressive equity), 7-9% (conservative/debt allocation) |

| Risk Level | Medium — depends on asset allocation choice (E/C/G) |

| Minimum Investment | ₹1,000/year (Tier I), ₹250/contribution |

| Tax on Returns | 60% of corpus tax-free at maturity; 40% must buy annuity (annuity income taxable) |

| Who It's Best For | Long-term retirement planners who want equity exposure with tax benefits |

For a 30-year-old investing ₹50,000/year in NPS with 75% equity allocation earning 10% CAGR, the projected corpus at age 60 would be approximately ₹1.05 crore. Of this, ₹63 lakh would be tax-free, and ₹42 lakh would go into an annuity.

InvestingPro Verdict: NPS is underrated. The additional ₹50,000 deduction under 80CCD(1B) saves another ₹15,600 (at 30% slab) on top of 80C savings. However, the mandatory annuity purchase and lock-in till 60 are downsides. Best used alongside PPF and ELSS, not as a replacement. Read our detailed NPS Tax Benefits Guide.

4. National Savings Certificate (NSC)

NSC is a post office savings instrument with a 5-year lock-in and guaranteed returns backed by the Government of India. It is a straightforward, no-frills option for conservative tax savers.

| Parameter | Details |

|---|---|

| Lock-in Period | 5 years |

| Current Interest Rate | 7.7% per annum (compounded annually) |

| Risk Level | Zero — sovereign guarantee |

| Minimum Investment | ₹1,000 (no maximum limit, but 80C deduction capped at ₹1.5 lakh) |

| Tax on Returns | Interest is taxable at slab rate, but accrued interest for years 1-4 qualifies as fresh 80C investment |

| Who It's Best For | Moderate-risk investors who want a guaranteed return and shorter lock-in than PPF |

A ₹1,50,000 investment in NSC at 7.7% matures to approximately ₹2,17,800 after 5 years. The interest earned is taxable, but accrued (reinvested) interest during years 1-4 can itself be claimed as 80C deduction in subsequent years — a unique advantage.

InvestingPro Verdict: NSC is a decent option if you want sovereign safety and a shorter lock-in than PPF. The reinvestment of interest qualifying as fresh 80C deduction is an underused benefit. However, the returns are lower than PPF and fully taxable on the interest component (except the reinvested years). Prefer PPF if you can handle the lock-in.

5. Tax-Saving Fixed Deposits (5-Year FD)

Tax-saving FDs are special 5-year fixed deposits offered by banks that qualify for 80C deduction. They work like regular FDs but come with a mandatory lock-in and no premature withdrawal option.

| Parameter | Details |

|---|---|

| Lock-in Period | 5 years (no premature withdrawal, no loan against deposit) |

| Expected Returns | 6.5-7.5% (varies by bank; senior citizens get 0.25-0.5% extra) |

| Risk Level | Very Low — bank deposit, covered under DICGC up to ₹5 lakh |

| Minimum Investment | ₹1,000-₹10,000 (varies by bank) |

| Tax on Returns | Interest fully taxable at slab rate. TDS deducted if interest > ₹40,000/year (₹50,000 for senior citizens) |

| Who It's Best For | Extremely risk-averse individuals, senior citizens seeking guaranteed income |

InvestingPro Verdict: Tax-saving FDs are the least efficient 80C option for most people. The returns are lower than PPF, NSC, and SCSS — and the interest is fully taxable. The only advantage is familiarity and convenience (your bank offers it). Choose PPF or NSC instead if you want safety. Browse current rates on our Fixed Deposits page.

6. Sukanya Samriddhi Yojana (SSY)

Sukanya Samriddhi Yojana is a government scheme exclusively for the girl child, offering the highest guaranteed interest rate among all small savings schemes. It combines tax-free returns with sovereign safety.

| Parameter | Details |

|---|---|

| Lock-in Period | 21 years from account opening (or marriage after 18); deposits required for first 15 years |

| Current Interest Rate | 8.2% per annum (highest among govt. schemes) |

| Risk Level | Zero — sovereign guarantee |

| Minimum Investment | ₹250/year (Max: ₹1,50,000/year) |

| Tax on Returns | Fully tax-free (EEE status) |

| Who It's Best For | Parents of a girl child below 10 years of age (maximum 2 accounts) |

Depositing ₹1,50,000 annually for 15 years at 8.2% interest rate builds a maturity corpus of approximately ₹69.3 lakh by the 21st year — completely tax-free. This is the best risk-free return available in India.

InvestingPro Verdict: If you have a daughter below 10, SSY should be a non-negotiable part of your 80C portfolio. At 8.2% tax-free, no other government scheme comes close. The long lock-in aligns perfectly with a child's education and marriage timeline.

7. Senior Citizens Savings Scheme (SCSS)

SCSS is designed specifically for individuals aged 60 and above (or 55+ for those who have taken VRS). It offers quarterly interest payouts, making it ideal for regular income needs in retirement.

| Parameter | Details |

|---|---|

| Lock-in Period | 5 years (extendable by 3 years) |

| Current Interest Rate | 8.2% per annum (paid quarterly) |

| Risk Level | Zero — sovereign guarantee |

| Minimum Investment | ₹1,000 (Max: ₹30 lakh per individual) |

| Tax on Returns | Interest taxable at slab rate. TDS deducted if interest > ₹50,000/year |

| Who It's Best For | Retirees needing regular quarterly income with safety |

InvestingPro Verdict: For anyone above 60, SCSS is the best 80C option. The 8.2% quarterly payout provides reliable income, and the 5-year lock-in is reasonable. Pair it with a Senior Citizen Tax-Saving FD for additional tax planning.

8. Life Insurance Premiums

Premiums paid for life insurance policies on yourself, spouse, or children qualify under Section 80C. This includes term insurance, endowment plans, and ULIPs.

| Parameter | Details |

|---|---|

| Lock-in Period | Policy term (minimum 5 years for deduction to apply) |

| Expected Returns | Term: 0% (pure protection); Endowment: 4-6%; ULIP: market-linked |

| Risk Level | Varies by product type |

| Minimum Investment | Varies by policy (term insurance: ₹500-800/month for ₹1 crore cover) |

| Tax on Returns | Maturity amount tax-free under Sec 10(10D) if annual premium is less than 10% of sum assured |

| Who It's Best For | Anyone with dependents who need life cover |

InvestingPro Verdict: Buy term insurance for protection — it is cheap, efficient, and essential if anyone depends on your income. But do not buy insurance for tax saving. Traditional endowment and money-back plans give poor returns (4-5%) while locking your money for 15-20 years. Invest in ELSS or PPF instead for the 80C deduction. Read our Term vs Whole Life Insurance comparison.

9. Home Loan Principal Repayment

The principal component of your home loan EMI qualifies for deduction under Section 80C. This also includes stamp duty and registration charges paid during the year of purchase.

| Parameter | Details |

|---|---|

| Lock-in | Property must not be sold within 5 years of possession — else deduction reversed |

| Deduction Scope | Principal portion of EMI + stamp duty + registration charges |

| Risk | N/A — this is an expense, not an investment |

| Who It's Best For | Home buyers with an active home loan |

On a ₹50 lakh home loan at 8.5% for 20 years (EMI ≈ ₹43,391/month), the principal repayment in the first year is approximately ₹1,00,000. This automatically counts toward your 80C limit. Plus, the interest component qualifies for a separate deduction of up to ₹2 lakh under Section 24(b).

InvestingPro Verdict: If you already have a home loan, your principal repayment automatically fills a chunk of the 80C limit. You do not need to make separate investments to that extent. Combine with the ₹2 lakh interest deduction under Section 24(b) for maximum benefit. See our Home Loan EMI Guide for detailed calculations.

10. Tuition Fees

Tuition fees paid for the full-time education of up to 2 children qualify under Section 80C. This covers school fees, college fees, and university fees in India.

| Parameter | Details |

|---|---|

| Eligible Expenses | Tuition fees only — not development fees, donation, transport, hostel, or books |

| Number of Children | Maximum 2 children per parent (both parents can claim for 2 each = 4 total) |

| Eligible Institutions | Any school, college, or university in India (not coaching/private tutoring) |

| Who It's Best For | Parents paying school or college fees |

InvestingPro Verdict: If you pay school fees, claim this deduction — it reduces the amount you need to invest separately. Many parents miss this. Keep fee receipts as proof. Note that both parents can claim for 2 children each if both are taxpayers, effectively covering 4 children in a family.

11. Employee Provident Fund (EPF)

For salaried employees, 12% of basic salary is automatically deducted as EPF contribution. This mandatory deduction qualifies under Section 80C. Many employees do not realize their 80C limit is already partially or fully consumed by EPF.

| Parameter | Details |

|---|---|

| Lock-in Period | Till retirement; withdrawal allowed after 2 months of unemployment or for specific purposes (home, medical, education) |

| Current Interest Rate | 8.25% per annum (FY 2025-26) |

| Risk Level | Zero — backed by Government of India |

| Contribution | 12% of basic salary (employee share); employer matches 12% (8.33% to pension, 3.67% to EPF) |

| Tax on Returns | Tax-free if service is 5+ years. Interest on contribution above ₹2.5 lakh/year is taxable |

| Who It's Best For | All salaried employees (mandatory) |

On a basic salary of ₹50,000/month, your annual EPF contribution is ₹72,000 (₹6,000 × 12). This means only ₹78,000 of the ₹1.5 lakh 80C limit remains for other investments.

InvestingPro Verdict: Check your payslip first. Your EPF contribution is already eating into the ₹1.5 lakh limit. If your basic salary is ₹1,04,167/month or more, your EPF alone exhausts the full 80C limit (₹12,500 × 12 = ₹1,50,000). In such cases, focus on 80CCD(1B) for NPS and 80D for health insurance instead.

₹ Salary-Based Tax Saving Scenarios

Knowing the options is not enough. What matters is how they apply to your salary level. Here are four real-world scenarios with complete math showing exactly how much you save and where to invest.

Scenario 1: ₹6 Lakh Annual Salary — No 80C Needed

If your gross salary is ₹6,00,000, you likely do not need 80C deductions at all.

| Component | New Tax Regime | Old Tax Regime |

|---|---|---|

| Gross Salary | ₹6,00,000 | ₹6,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| 80C Deductions | Not available | ₹1,50,000 (if invested) |

| Taxable Income | ₹5,25,000 | ₹4,00,000 |

| Tax Before Rebate | ₹27,500 | ₹7,500 |

| Rebate u/s 87A | ₹27,500 (full waiver up to ₹7L) | ₹5,000 (up to ₹5L taxable) |

| Tax Payable | ₹0 | ₹2,500 + cess = ₹2,600 |

Verdict: At ₹6 lakh salary, the New Tax Regime gives you zero tax without any investment. There is no reason to lock up ₹1.5 lakh in 80C investments just for tax saving. Invest based on your financial goals, not for tax benefits.

Scenario 2: ₹10 Lakh Annual Salary — Smart 80C Allocation

At ₹10 lakh, 80C deductions start making a meaningful difference. Here is an optimized allocation:

| Investment | Amount | Rationale |

|---|---|---|

| EPF (auto-deducted, basic ₹40,000/month) | ₹57,600 | Mandatory, no action needed |

| ELSS SIP (₹5,000/month) | ₹60,000 | Wealth creation, shortest lock-in |

| PPF | ₹32,400 | Safe, tax-free, long-term |

| Total 80C | ₹1,50,000 |

| Component | Old Tax Regime | New Tax Regime |

|---|---|---|

| Gross Salary | ₹10,00,000 | ₹10,00,000 |

| Standard Deduction | ₹50,000 | ₹75,000 |

| 80C Deduction | ₹1,50,000 | ₹0 |

| 80D (Health Insurance) | ₹25,000 | ₹0 |

| Taxable Income | ₹7,75,000 | ₹9,25,000 |

| Tax + Cess | ₹59,800 | ₹68,900 |

| Tax Saved with Old Regime | ₹9,100 | |

Verdict: At ₹10 lakh, the Old Regime with ₹1.75 lakh in deductions (80C + 80D) saves about ₹9,100. The margin is slim — if you do not have HRA or home loan interest to claim, the New Regime may be just as good. Use our Tax Calculator with your exact numbers.

Scenario 3: ₹15 Lakh Annual Salary — Maximum Optimization

At ₹15 lakh, the Old Tax Regime with full deductions clearly wins. Here is an optimized allocation combining 80C with other sections:

| Deduction | Section | Amount |

|---|---|---|

| EPF (basic ₹60,000/month) | 80C | ₹86,400 |

| ELSS SIP (₹4,000/month) | 80C | ₹48,000 |

| PPF | 80C | ₹15,600 |

| Total 80C | 80C | ₹1,50,000 |

| NPS (additional) | 80CCD(1B) | ₹50,000 |

| Health Insurance (self + parents) | 80D | ₹50,000 |

| Home Loan Interest | 24(b) | ₹2,00,000 |

| HRA Exemption | 10(13A) | ₹1,80,000 |

| Total Deductions | ₹6,30,000 |

| Component | Old Tax Regime | New Tax Regime |

|---|---|---|

| Gross Salary | ₹15,00,000 | ₹15,00,000 |

| Total Deductions | ₹6,80,000 (incl. ₹50K std. deduction) | ₹75,000 (std. deduction only) |

| Taxable Income | ₹8,20,000 | ₹14,25,000 |

| Tax + Cess | ₹73,840 | ₹1,63,800 |

| Tax Saved with Old Regime | ₹89,960 | |

Verdict: At ₹15 lakh with a home loan and full deductions, you save nearly ₹90,000 per year by choosing the Old Regime. The combination of 80C + NPS + health insurance + home loan interest creates a powerful tax shield.

Scenario 4: ₹25 Lakh Annual Salary — Aggressive Tax Optimization

At ₹25 lakh, you are in the 30% tax bracket. Every deduction saves you ₹31.20 for every ₹100 claimed (30% + 4% cess). Here is the full optimization strategy:

| Deduction | Section | Amount | Tax Saved (at 30%+cess) |

|---|---|---|---|

| EPF + ELSS + PPF | 80C | ₹1,50,000 | ₹46,800 |

| NPS additional | 80CCD(1B) | ₹50,000 | ₹15,600 |

| Health Insurance (self + parents senior) | 80D | ₹75,000 | ₹23,400 |

| Home Loan Interest | 24(b) | ₹2,00,000 | ₹62,400 |

| HRA Exemption | 10(13A) | ₹3,00,000 | ₹93,600 |

| Standard Deduction | 16(ia) | ₹50,000 | ₹15,600 |

| Total Deductions | ₹8,25,000 | ₹2,57,400 |

| Component | Old Tax Regime | New Tax Regime |

|---|---|---|

| Gross Salary | ₹25,00,000 | ₹25,00,000 |

| Total Deductions | ₹8,25,000 | ₹75,000 |

| Taxable Income | ₹16,75,000 | ₹24,25,000 |

| Tax + Cess | ₹2,76,120 | ₹4,63,320 |

| Tax Saved with Old Regime | ₹1,87,200 | |

Verdict: At ₹25 lakh salary with full deductions, the Old Regime saves you ₹1.87 lakh in taxes — that is an entire month's in-hand salary. The key is stacking deductions across multiple sections, not just 80C alone. Also read our comprehensive guide on How to Save Tax on Salary Income.

80C Allocation Strategy by Life Stage

Your ideal 80C portfolio changes as you age. What works for a 28-year-old first-jobber is wrong for a 55-year-old nearing retirement. Here are recommended allocations by life stage.

Young Professional (Age 25-35, Single or Newly Married)

| Investment | Allocation | Amount (of ₹1.5L) | Why |

|---|---|---|---|

| EPF (auto-deducted) | 30-40% | ₹45,000-60,000 | Mandatory, builds retirement base |

| ELSS SIP | 40-50% | ₹60,000-75,000 | Wealth creation, highest growth potential |

| PPF | 10-20% | ₹15,000-30,000 | Debt anchor, tax-free compounding |

| Term Insurance Premium | 5-10% | ₹7,500-15,000 | Essential protection if dependents exist |

Focus: Maximize equity allocation. You have 25-30 years for compounding. ELSS should be the largest voluntary component. Start PPF early — by 50, you will have a substantial tax-free corpus.

Family Person (Age 35-45, Kids in School)

| Investment | Allocation | Amount (of ₹1.5L) | Why |

|---|---|---|---|

| EPF (auto-deducted) | 35-45% | ₹52,000-67,000 | Mandatory, growing with salary |

| Children's Tuition Fees | 15-25% | ₹22,000-37,000 | Already spending this — claim it |

| Home Loan Principal | 15-25% | ₹22,000-37,000 | Already paying EMI — auto-qualifies |

| ELSS SIP | 10-20% | ₹15,000-30,000 | Continued equity exposure |

| SSY (if daughter) | 10-15% | ₹15,000-22,000 | Tax-free, highest govt. rate |

| Term Insurance | 5% | ₹7,500 | Non-negotiable at this stage |

Focus: At this stage, EPF + tuition fees + home loan principal may already exhaust your ₹1.5 lakh limit. If so, you do not need additional 80C investments. Redirect surplus to NPS (80CCD(1B)) and health insurance (80D) instead.

Pre-Retirement (Age 50-58)

| Investment | Allocation | Amount (of ₹1.5L) | Why |

|---|---|---|---|

| EPF (auto-deducted) | 50-60% | ₹75,000-90,000 | Higher basic salary = higher EPF |

| PPF | 20-30% | ₹30,000-45,000 | Extend existing PPF; safe, tax-free |

| NSC | 10-15% | ₹15,000-22,000 | 5-year lock-in suits timeline |

| Term Insurance | 5% | ₹7,500 | Maintain cover till 60 |

Focus: Shift away from equity toward guaranteed instruments. Your EPF at this salary level likely covers most of the 80C limit. Extend PPF accounts in 5-year blocks. Avoid new ELSS if you plan to retire within 5 years.

Senior Citizen (Age 60+)

| Investment | Allocation | Amount (of ₹1.5L) | Why |

|---|---|---|---|

| SCSS | 50-60% | ₹75,000-90,000 | 8.2% quarterly income, sovereign safety |

| Tax-Saving FD | 20-30% | ₹30,000-45,000 | Convenient, extra 0.5% senior rate |

| PPF (extension) | 10-20% | ₹15,000-30,000 | Tax-free returns, liquid after 15-year maturity |

Focus: Capital preservation and regular income. SCSS provides quarterly payouts. Avoid equity (ELSS) and long lock-in instruments. PPF extensions (without fresh deposits) still earn tax-free interest.

Beyond 80C — Stack More Deductions

Section 80C is just the starting point. Smart taxpayers combine multiple sections to reduce taxable income significantly. Here are the most important deductions beyond 80C.

| Section | Deduction For | Maximum Limit | Available in New Regime? |

|---|---|---|---|

| 80CCD(1B) | NPS additional contribution | ₹50,000 | No |

| 80D | Health insurance premium (self + family + parents) | ₹25,000 self + ₹25,000 parents (₹50,000 if parents are senior citizens) | No |

| 80E | Interest on education loan | No limit (for 8 years from start of repayment) | No |

| Section 24(b) | Home loan interest (self-occupied property) | ₹2,00,000 | No |

| 80TTA | Interest from savings accounts | ₹10,000 | No |

| 80TTB | Interest income for senior citizens (all deposits) | ₹50,000 | No |

| 80G | Donations to approved charities | 50% or 100% of donation (varies by charity) | No |

| 80GG | Rent paid (if HRA not received) | ₹5,000/month or 25% of total income (lower of the two) | No |

Maximum stacking example: 80C (₹1.5L) + 80CCD(1B) (₹50K) + 80D (₹75K) + 24(b) (₹2L) + HRA (variable) = ₹4.75 lakh+ in deductions before HRA. This is why the Old Tax Regime often wins for salaried employees with loans and insurance.

5 Common Tax Saving Mistakes to Avoid

Claiming 80C is straightforward, but these mistakes cost thousands of rupees every year. Avoid them.

1. Investing the entire ₹1.5 lakh in March. This is the most common mistake. Investing a lump sum in March means you buy ELSS at whatever price the market offers, miss 11 months of compounding, and make decisions under time pressure. Start a SIP in April. Spread PPF deposits across the year (deposit before the 5th of each month to earn interest for that month).

2. Not checking EPF contribution before investing. If your basic salary is ₹62,500/month or more, your EPF contribution alone is ₹90,000/year — that is 60% of the 80C limit already consumed. Many people invest the full ₹1.5 lakh separately and realize too late that their total exceeds the deductible limit. The excess gets no tax benefit and is just locked money.

3. Buying insurance for tax saving instead of protection. Endowment plans, money-back policies, and ULIPs are sold aggressively as "tax-saving" products. They offer 4-6% returns while locking your money for 15-25 years. A ₹1 crore term insurance costs only ₹8,000-12,000/year. Buy term insurance for protection, invest the rest in ELSS or PPF for tax saving. Never mix insurance and investment.

4. Choosing the wrong tax regime without calculating. Many taxpayers default to the New Regime because it is simpler, even when the Old Regime with deductions would save them more. Others stick to the Old Regime out of habit when they do not have enough deductions to justify it. Calculate both scenarios using our Tax Calculator before deciding. Salaried employees can switch between regimes every year.

5. Ignoring deductions beyond 80C. Section 80C is a ₹1.5 lakh cap. But 80CCD(1B) adds ₹50,000, 80D adds up to ₹75,000, and Section 24(b) adds ₹2 lakh. Together, these sections can save an additional ₹1 lakh+ in taxes for someone in the 30% bracket. Do not stop at 80C — build a complete deduction portfolio.

Step-by-Step: How to Claim 80C Deductions

If you are a salaried employee, here is the exact process to claim your 80C deductions correctly and avoid scrutiny.

Step 1: Declare investments at the start of the financial year (April-May). Your employer sends an investment declaration form. Fill in your planned 80C investments (ELSS, PPF, LIC, etc.), 80D health insurance, home loan details, and HRA. Your employer will calculate TDS based on these declarations, reducing monthly tax deduction.

Step 2: Make the actual investments throughout the year. Start ELSS SIPs in April. Make PPF deposits monthly (before the 5th). Pay insurance premiums on time. Keep all receipts and transaction records.

Step 3: Submit investment proofs to your employer (January-February). Your employer asks for proof of actual investments. Submit: PPF passbook copy, ELSS mutual fund statement, life insurance premium receipts, home loan interest certificate from bank, children's school fee receipts, NPS transaction statement, and health insurance premium receipt.

Step 4: Receive Form 16 (May-June after financial year ends). Your employer issues Form 16 showing total salary, TDS deducted, and deductions claimed. Verify that all your 80C investments are reflected correctly. If any deduction is missing, you can still claim it in your ITR.

Step 5: File your Income Tax Return. File ITR on the income tax portal (incometax.gov.in) before July 31. Choose ITR-1 (for salary income up to ₹50 lakh) or ITR-2 (if you have capital gains). Enter all deductions under Schedule VI-A. The system auto-populates some data from Form 16 and Form 26AS/AIS.

Step 6: Keep records for 6 years. Maintain investment proofs, receipts, and bank statements for at least 6 years from the end of the assessment year. The IT department can reopen cases within this period.

Frequently Asked Questions

Can I claim Section 80C deductions under the New Tax Regime?

No. Section 80C deductions are not available under the New Tax Regime (Section 115BAC). The New Regime offers lower slab rates but removes most deductions including 80C, 80D, HRA, and home loan interest. Only the standard deduction of ₹75,000 and employer NPS contribution (80CCD(2)) are available. You must opt for the Old Tax Regime to claim 80C. Salaried employees can switch between regimes every financial year.

Is the ₹1.5 lakh 80C limit per person or per family?

The ₹1,50,000 limit is per individual taxpayer, not per family. Both spouses can independently claim up to ₹1.5 lakh each under their own PAN. This means a couple can claim a combined ₹3 lakh in 80C deductions if both are taxpayers. However, the same investment cannot be claimed by two people — for instance, if the husband pays the LIC premium, only he can claim the deduction, not the wife.

My EPF contribution already exhausts the ₹1.5 lakh limit. Should I still invest in ELSS or PPF?

If your EPF employee contribution (12% of basic) equals or exceeds ₹1,50,000 per year (basic salary ≥ ₹1,04,167/month), then you do not need any additional 80C investments for tax saving. However, ELSS and PPF are good investments in their own right. ELSS offers equity growth with a short 3-year lock-in, and PPF offers tax-free guaranteed returns. Invest in them for wealth creation, not just for tax saving. Also, redirect your tax-saving focus to 80CCD(1B) for an extra ₹50,000 NPS deduction and 80D for health insurance premiums.

Can I invest more than ₹1.5 lakh in PPF?

No. The maximum annual deposit in PPF is ₹1,50,000. Any amount deposited beyond this limit will not earn interest and will be returned. You also cannot claim deduction beyond ₹1.5 lakh under 80C. If you want to invest more in risk-free instruments, consider NSC (no upper limit on investment, though 80C benefit is capped), RBI Floating Rate Bonds, or SCSS (if eligible).

What is the last date to make 80C investments for FY 2025-26?

The deadline is March 31, 2026. All 80C qualifying investments and expenses must be made or paid between April 1, 2025 and March 31, 2026 to claim deductions for FY 2025-26 (AY 2026-27). However, do not wait until March. Start early in April to benefit from full-year compounding, rupee-cost averaging (for ELSS SIPs), and avoid last-minute rush decisions.

Do I need to submit investment proofs to the IT department?

Not at the time of filing your ITR. The Income Tax Department works on a self-assessment basis — you declare your deductions in the ITR, and the department may ask for proof during scrutiny or assessment. However, you must submit proofs to your employer (typically in January-February) for correct TDS calculation. Keep all proofs — PPF passbook, ELSS statements, insurance receipts, school fee receipts, home loan certificates — for at least 6 years from the end of the assessment year.

ELSS vs PPF — which is better for tax saving?

It depends on your risk appetite and time horizon. ELSS is better if: you are under 45, you are comfortable with equity volatility, you want the shortest lock-in (3 years), and you want higher returns (12-15% historically). PPF is better if: you are risk-averse, you want guaranteed tax-free returns (7.1%), and you do not need the money for 15 years. The best approach is to split — invest 60-70% in ELSS and 30-40% in PPF. This gives you growth potential with a safety net. Read our detailed analysis: Best ELSS Funds for 2026.

Can NRIs claim Section 80C deductions?

Yes, partially. NRIs can claim 80C deductions on: life insurance premiums, tuition fees for children studying in India, home loan principal repayment for property in India, and NSC/ELSS investments. However, NRIs cannot open new PPF accounts (existing accounts can continue till maturity). NRIs can invest in ELSS on a repatriation basis. The deduction is available only if the NRI has taxable income in India and files an Indian tax return under the Old Tax Regime.

What about freelancers and self-employed individuals?

Self-employed individuals and freelancers can claim Section 80C deductions on the same investments as salaried employees — ELSS, PPF, NSC, life insurance, tuition fees, home loan principal. The key differences: (1) There is no EPF — you can invest in PPF up to ₹1.5 lakh to replicate the safety of EPF. (2) There is no employer NPS contribution — but you can claim both 80CCD(1) within 80C and 80CCD(1B) additionally. (3) You must choose between Old and New Regime when filing ITR (ITR-3 or ITR-4). (4) Self-employed individuals have more flexibility in structuring their income and deductions compared to salaried employees.

What is the difference between Section 80C, 80CCC, and 80CCD?

All three fall under the combined ₹1.5 lakh limit of Section 80CCE, but they cover different instruments:

- Section 80C: Covers the broadest range — ELSS, PPF, NSC, tax-saving FD, SSY, SCSS, EPF, life insurance, home loan principal, tuition fees, and stamp duty.

- Section 80CCC: Covers contributions to pension funds of LIC or other insurers (e.g., Jeevan Suraksha). This is rarely used now as NPS has replaced most pension products.

- Section 80CCD(1): Covers your own contribution to NPS. This falls within the ₹1.5 lakh combined limit of 80C + 80CCC + 80CCD(1).

- Section 80CCD(1B): This is the bonus — an additional ₹50,000 deduction for NPS over and above the ₹1.5 lakh limit. This is the only way to get a tax deduction beyond 80C for retirement savings.

- Section 80CCD(2): Employer's NPS contribution (up to 14% of basic for government employees, 10% for others). This is outside the ₹1.5 lakh limit and available even under the New Tax Regime.

Disclaimer

This article is for educational purposes only and does not constitute tax advice. Tax laws are subject to change based on government notifications and amendments. All information is based on the Income Tax Act as applicable for FY 2025-26 (AY 2026-27). Tax calculations are approximate and may vary based on individual circumstances including HRA, special allowances, and other income sources. Please consult a qualified Chartered Accountant (CA) or tax advisor for personalized tax planning advice specific to your situation. InvestingPro.in does not guarantee the accuracy of tax calculations and is not liable for any financial decisions made based on this article.