The bank says you are eligible for Rs 80 lakh. You think you can afford it. Then the EMI starts and suddenly Rs 65,000 per month feels very different from what you imagined. Let us do the real math.

Most home buyers in India make one critical mistake. They confuse what the bank will lend them with what they can actually afford. These are two very different numbers. The bank looks at your salary slip and calculates a maximum. Your life looks at your groceries, school fees, car EMI, parents' medical bills, and that annual vacation you refuse to give up.

This guide will walk you through the EMI formula, show you exactly how much interest you will pay over the life of your loan, explain how banks decide your interest rate, and most importantly, help you figure out what you can genuinely afford without eating dal-chawal for 20 years.

The EMI Formula: How Banks Calculate Your Monthly Payment

Every home loan EMI in India is calculated using one formula. Whether it is SBI, HDFC, ICICI, or any other bank, the math is the same:

EMI = P x r x (1+r)^n / [(1+r)^n - 1]

Where:

- P = Principal loan amount (the amount you borrow)

- r = Monthly interest rate (annual rate divided by 12)

- n = Total number of monthly installments (tenure in years x 12)

Let us work through a real example.

Worked Example: Rs 50 Lakh Loan at 8.5% for 20 Years

- P = Rs 50,00,000

- Annual interest rate = 8.5%, so r = 8.5 / 12 / 100 = 0.007083

- Tenure = 20 years, so n = 20 x 12 = 240 months

Plugging into the formula:

EMI = 50,00,000 x 0.007083 x (1.007083)^240 / [(1.007083)^240 - 1]

Let us calculate (1.007083)^240 = 5.4318

EMI = 50,00,000 x 0.007083 x 5.4318 / [5.4318 - 1]

EMI = 50,00,000 x 0.03848 / 4.4318

EMI = 1,92,400 / 4.4318

EMI = Rs 43,391 per month

Over 20 years, you will pay 43,391 x 240 = Rs 1,04,13,840. That is Rs 54,13,840 in interest alone, which is more than the original loan amount. This is why understanding the numbers matters before you sign.

You do not need to do this math by hand. Use our Home Loan EMI Calculator to get instant results for any combination of loan amount, interest rate, and tenure.

How to Use Our Home Loan EMI Calculator

Our Home Loan EMI Calculator is designed to give you more than just a monthly number. Here is how to get the most out of it:

Step 1: Enter Your Loan Amount

Slide the bar or type in the total home loan amount you plan to borrow. Remember, this is the loan amount, not the property price. If the flat costs Rs 70 lakh and you are putting Rs 20 lakh as down payment, your loan amount is Rs 50 lakh.

Step 2: Set the Interest Rate

Enter the interest rate your bank has offered. If you have not spoken to a bank yet, use 8.5% as a baseline. That is roughly the average across major banks in 2026. Check our Home Loan Interest Rates: All Banks 2026 guide for the latest rates.

Step 3: Choose Your Tenure

Select the repayment period in years. Most banks offer 5 to 30 years. The sweet spot for most borrowers is 15 to 20 years. Going beyond 20 years adds relatively little to affordability but significantly increases total interest.

Step 4: Read the Results

The calculator shows your monthly EMI, total interest payable, total amount payable (principal + interest), and an amortization chart that shows how much of each EMI goes toward principal versus interest over time. In the early years, nearly 70-80% of your EMI is just interest. The principal repayment only picks up speed after year 8-10.

EMI Tables for Popular Loan Amounts

Here are pre-calculated EMI tables so you can quickly reference what your monthly payment would look like. All figures are in rupees.

15-Year Tenure

| Loan Amount | 8.00% | 8.50% | 9.00% | 9.50% |

|---|---|---|---|---|

| Rs 20 Lakh | 19,113 | 19,714 | 20,285 | 20,868 |

| Rs 30 Lakh | 28,670 | 29,571 | 30,428 | 31,302 |

| Rs 50 Lakh | 47,783 | 49,285 | 50,713 | 52,170 |

| Rs 75 Lakh | 71,674 | 73,928 | 76,070 | 78,255 |

| Rs 1 Crore | 95,565 | 98,570 | 1,01,427 | 1,04,340 |

20-Year Tenure

| Loan Amount | 8.00% | 8.50% | 9.00% | 9.50% |

|---|---|---|---|---|

| Rs 20 Lakh | 16,729 | 17,356 | 17,995 | 18,643 |

| Rs 30 Lakh | 25,093 | 26,035 | 26,992 | 27,965 |

| Rs 50 Lakh | 41,822 | 43,391 | 44,986 | 46,608 |

| Rs 75 Lakh | 62,733 | 65,087 | 67,480 | 69,912 |

| Rs 1 Crore | 83,644 | 86,782 | 89,973 | 93,216 |

25-Year Tenure

| Loan Amount | 8.00% | 8.50% | 9.00% | 9.50% |

|---|---|---|---|---|

| Rs 20 Lakh | 15,440 | 16,105 | 16,782 | 17,468 |

| Rs 30 Lakh | 23,160 | 24,158 | 25,173 | 26,202 |

| Rs 50 Lakh | 38,600 | 40,263 | 41,955 | 43,670 |

| Rs 75 Lakh | 57,900 | 60,395 | 62,933 | 65,505 |

| Rs 1 Crore | 77,200 | 80,527 | 83,910 | 87,340 |

30-Year Tenure

| Loan Amount | 8.00% | 8.50% | 9.00% | 9.50% |

|---|---|---|---|---|

| Rs 20 Lakh | 14,676 | 15,376 | 16,089 | 16,813 |

| Rs 30 Lakh | 22,013 | 23,064 | 24,134 | 25,219 |

| Rs 50 Lakh | 36,689 | 38,440 | 40,224 | 42,032 |

| Rs 75 Lakh | 55,033 | 57,660 | 60,335 | 63,048 |

| Rs 1 Crore | 73,376 | 76,880 | 80,447 | 84,064 |

Notice something? Going from 20 years to 30 years reduces your EMI by only Rs 5,000-10,000 on a Rs 50 lakh loan. But the extra 10 years of interest payments add up to Rs 15-25 lakh more. That is why blindly choosing the longest tenure is almost always a bad idea.

The Real Cost: Total Interest You Will Pay

This is the table most banks will not show you voluntarily. It reveals the total interest you pay over the full loan tenure, expressed as a percentage of the principal.

| Tenure | Rate | Total Interest on Rs 50 Lakh | Interest as % of Principal |

|---|---|---|---|

| 15 years | 8.5% | Rs 38.71 Lakh | 77% |

| 20 years | 8.5% | Rs 54.14 Lakh | 108% |

| 25 years | 8.5% | Rs 70.79 Lakh | 142% |

| 30 years | 8.5% | Rs 88.18 Lakh | 176% |

| 20 years | 9.0% | Rs 57.97 Lakh | 116% |

| 20 years | 9.5% | Rs 61.86 Lakh | 124% |

Read that again. On a 20-year loan at 8.5%, you pay Rs 54 lakh in interest on a Rs 50 lakh loan. You are essentially paying for the house twice. At 30 years, you pay Rs 88 lakh in interest, nearly 1.76 times the original loan. This is not a reason to avoid home loans entirely. It is a reason to be strategic about tenure, prepayments, and the interest rate you negotiate.

MCLR vs repo rate: How Your Interest Rate is Decided

If you have compared home loan offers, you have seen two terms: MCLR-linked and repo rate-linked (also called external benchmark-linked or EBLR). Understanding the difference directly affects how much you pay.

MCLR-Linked Loans

MCLR stands for Marginal Cost of Funds Based Lending Rate. Banks calculate MCLR based on their internal cost of deposits, operating costs, and profit margins. Your home loan rate is typically MCLR + a spread (for example, MCLR 8.0% + spread 0.25% = 8.25%).

How rate changes work: Banks review MCLR monthly but your loan rate resets only on your reset date, which is usually once a year. So if the RBI cuts rates in January but your reset date is in June, you wait until June to benefit. This delay can cost you several months of higher EMI.

repo rate-Linked Loans (EBLR)

Since October 2019, RBI mandated that all new floating-rate retail loans must be linked to an external benchmark. Most banks use the RBI repo rate. Your loan rate = Repo rate + bank's spread + risk premium (for example, 6.50% + 2.25% = 8.75%).

How rate changes work: Banks must reset your rate at least once every three months. So when RBI cuts the repo rate, your EMI drops within 3 months, not 12. This is significantly faster and more transparent.

Which Is Better?

For new borrowers in 2026, you almost certainly have a repo rate-linked loan, as that is now the standard. The advantage is faster transmission of rate cuts. The disadvantage is that rate hikes also hit you faster. If you still have an old MCLR-linked loan, consider asking your bank about switching to repo rate-linked. There may be a small conversion fee (Rs 5,000-10,000), but the transparency and faster rate reductions usually make it worthwhile.

Current repo rate as of early 2026 is 6.25%, following two consecutive cuts by RBI. This has brought most bank home loan rates into the 8.25-8.75% range. Track the latest rates in our complete bank-wise rate comparison.

5 Hidden Costs Beyond EMI That Nobody Tells You

Your EMI is not your only cost. Here are five expenses that catch almost every first-time home buyer off guard. Together, they add 8-12% on top of the property value.

1. Processing Fee: 0.5-1% of Loan Amount

Banks charge a processing fee to evaluate and sanction your loan. On a Rs 50 lakh loan, this is Rs 25,000 to Rs 50,000. Some banks offer processing fee waivers during festive seasons or for specific salary accounts. Always negotiate this.

2. Stamp Duty: 5-8% of Property Value

This is the biggest hidden cost and varies by state. In Maharashtra, stamp duty is 6% (5% stamp duty + 1% metro cess in Mumbai/Pune). In Karnataka, it is 5%. In Delhi, it ranges from 4-6% depending on gender. On a Rs 70 lakh property, stamp duty in Maharashtra is Rs 4.2 lakh. Women buyers often get a 1-2% concession, so always register in the woman's name if possible.

Use our Stamp Duty Calculator to find the exact amount for your state.

3. Registration Charges: 1% of Property Value

On top of stamp duty, you pay a registration fee, typically 1% of the property value, capped at Rs 30,000 in some states. For our Rs 70 lakh example, that is another Rs 30,000 to Rs 70,000.

4. home loan Insurance: Rs 15,000-50,000 per Year

Banks push hard for home loan protection insurance, which pays off the remaining loan if you die during the tenure. While not legally mandatory, banks make it practically difficult to refuse. A separate term insurance policy is almost always cheaper. For a Rs 50 lakh cover, a term plan costs Rs 8,000-12,000 per year versus the bank's bundled plan at Rs 25,000-50,000.

5. GST on Processing Fee: 18%

Yes, there is GST on the processing fee. So that Rs 50,000 processing fee actually becomes Rs 59,000. GST also applies to insurance premiums, legal charges, and valuation fees.

Total Add-On Cost Example

For a Rs 70 lakh property with Rs 50 lakh loan:

| Cost | Amount |

|---|---|

| Stamp duty (6%) | Rs 4,20,000 |

| Registration (1%) | Rs 70,000 |

| Processing fee (0.5%) | Rs 25,000 |

| GST on processing fee | Rs 4,500 |

| Legal and valuation fees | Rs 15,000 |

| Insurance (year 1) | Rs 25,000 |

| Total | Rs 5,59,500 |

That is nearly Rs 5.6 lakh in costs that are not part of your EMI. Add this to your down payment when planning your budget.

Pre-Payment Strategy: How to Save Rs 15-25 Lakh

This is the most powerful section in this guide. Prepayment is the single best financial move you can make once you have a home loan. Here is why, with real numbers.

Scenario: Rs 50 Lakh Loan at 8.5% for 20 Years

Base case: EMI of Rs 43,391. Total interest = Rs 54.14 lakh. Total payout = Rs 1.04 crore.

Strategy 1: Pay Rs 5,000 Extra Every Month

By adding just Rs 5,000 to your monthly EMI (total Rs 48,391), here is what happens:

- Loan closes in 16 years 4 months instead of 20 years

- Total interest paid: Rs 41.8 lakh

- You save Rs 12.3 lakh in interest

- You get 3 years and 8 months of EMI-free life

Strategy 2: Annual Bonus as Prepayment

Suppose you put Rs 1 lakh from your annual bonus toward prepayment every year:

- Loan closes in 15 years 9 months instead of 20 years

- Total interest paid: Rs 39.2 lakh

- You save Rs 14.9 lakh in interest

Strategy 3: Both Combined

Rs 5,000 extra monthly + Rs 1 lakh annual bonus:

- Loan closes in 13 years 2 months instead of 20 years

- Total interest paid: Rs 30.6 lakh

- You save Rs 23.5 lakh in interest

- You reclaim nearly 7 years of monthly payments

The reason prepayment works so well is simple: in the early years of a loan, 70-80% of your EMI goes toward interest. Any extra payment goes directly toward reducing the principal, which reduces the base on which future interest is calculated. The earlier you start, the more you save.

Important: Check Prepayment Charges

Under RBI rules, banks cannot charge prepayment penalties on floating-rate home loans. This applies to all scheduled commercial banks and housing finance companies. If your bank tries to charge you for prepaying a floating-rate loan, they are violating RBI guidelines. Fixed-rate loans may have prepayment charges of 2-3%, which is one more reason floating rate is almost always better for home loans.

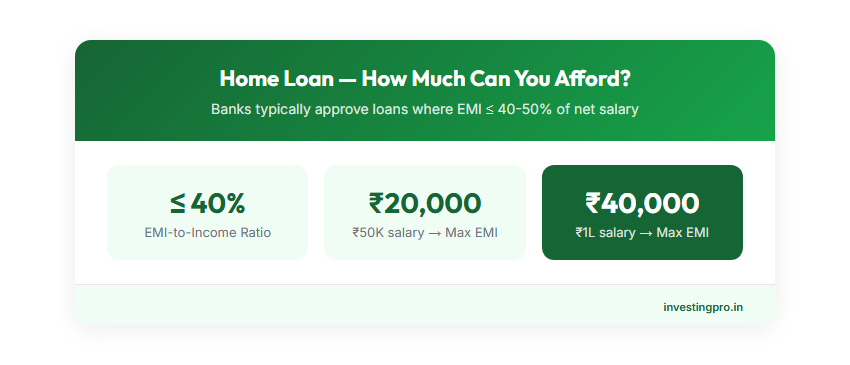

How Much Home Loan Can You Actually Afford?

Banks use a metric called FOIR (Fixed Obligation to Income Ratio) to decide your maximum eligible loan. Most banks cap FOIR at 50-60%. This means if your monthly income is Rs 1,00,000, the bank says your total EMIs (home loan + car loan + credit card minimum payments + personal loan) should not exceed Rs 50,000-60,000.

But bank eligibility and real affordability are different things.

The 50/30/20 Rule for Home Loans

A more realistic framework:

- 50% of take-home salary goes to needs (rent/EMI, groceries, utilities, insurance, school fees)

- 30% goes to wants (dining out, entertainment, travel, shopping)

- 20% goes to savings and investments (mutual funds, emergency fund, retirement)

Under this framework, your home loan EMI should be a subset of the 50% needs bucket. Since that bucket also includes groceries, utilities, and other fixed expenses, a realistic EMI allocation is 30-35% of your take-home salary.

Affordability Example

| Monthly Take-Home | Max Comfortable EMI (35%) | Max Loan at 8.5% for 20 Years | Approximate Property Budget (with 20% down) |

|---|---|---|---|

| Rs 60,000 | Rs 21,000 | Rs 24.2 Lakh | Rs 30 Lakh |

| Rs 80,000 | Rs 28,000 | Rs 32.3 Lakh | Rs 40 Lakh |

| Rs 1,00,000 | Rs 35,000 | Rs 40.3 Lakh | Rs 50 Lakh |

| Rs 1,50,000 | Rs 52,500 | Rs 60.5 Lakh | Rs 75 Lakh |

| Rs 2,00,000 | Rs 70,000 | Rs 80.7 Lakh | Rs 1 Crore |

Compare this with what the bank tells you. If your take-home is Rs 1 lakh, the bank may approve Rs 60-70 lakh. But a sustainable loan based on 35% EMI-to-income is closer to Rs 40 lakh. That Rs 20-30 lakh gap is where financial stress lives.

If you have a working spouse, use combined income. But stress-test with one income. What happens if one of you loses a job or takes a break for a child? Can you manage the EMI on a single salary for 6-12 months?

Rent vs Buy: Should You Even Take a Home Loan?

This is a question that divides Indian families like nothing else. Your parents say buy. Your Twitter feed says rent and invest. The truth is somewhere in the middle, and it depends entirely on numbers specific to your city.

The Price-to-Rent Ratio

Divide the property price by annual rent. If the result is:

- Below 15: Buying is clearly better

- 15 to 20: Could go either way, depends on your situation

- Above 20: Renting and investing the difference is likely better

In most Indian metros, this ratio is 25-35 for comparable properties. A flat that costs Rs 1 crore rents for Rs 25,000-30,000 per month. The price-to-rent ratio is 28-33, which strongly favors renting from a pure numbers perspective.

But numbers are not everything. Owning your home provides stability, the freedom to modify your space, no landlord drama, and a forced savings mechanism. These have real value that spreadsheets cannot capture.

Use our Rent vs Buy Calculator to run the numbers for your specific situation. It factors in rent escalation, property appreciation, investment returns, tax benefits, and maintenance costs.

For a deeper comparison with stamp duty, opportunity cost, and city-wise data, check the Rent vs Buy Detailed Comparison.

Frequently Asked Questions

How is home loan EMI calculated?

Home loan EMI is calculated using the reducing balance method with the formula: EMI = P x r x (1+r)^n / [(1+r)^n - 1], where P is the principal, r is the monthly interest rate (annual rate / 12 / 100), and n is the total number of monthly installments. In the early years, a larger portion of your EMI goes toward interest. As the principal reduces, more of each EMI goes toward repaying the actual loan.

Are there prepayment charges on home loans?

For floating-rate home loans, RBI has mandated that banks cannot charge any prepayment penalty. This applies to all scheduled commercial banks and housing finance companies. For fixed-rate home loans, banks may charge 2-3% of the prepaid amount as penalty. Since over 95% of home loans in India are floating rate, most borrowers can prepay freely without any charges.

What is the difference between floating and fixed interest rate?

A floating rate changes with market conditions. When the RBI adjusts the repo rate, your loan rate and EMI change accordingly. A fixed rate stays the same for the entire loan tenure or a specified period. In India, truly fixed-rate home loans are rare. Most so-called fixed rates are only fixed for 2-5 years and then convert to floating. Floating rates are usually 0.5-1% lower than fixed rates and offer free prepayment, making them the better choice for most borrowers.

What is the maximum tenure for a home loan?

Most banks offer home loans for up to 30 years. However, the loan must be repaid before you turn 60-65 (retirement age). So if you are 40, the maximum tenure may be capped at 20-25 years depending on the bank. SBI, HDFC, and ICICI all offer up to 30 years for younger borrowers. Note that longer tenure means lower EMI but significantly higher total interest. A 30-year loan costs 60-70% more in total interest compared to a 15-year loan.

Can my EMI change after taking a home loan?

Yes, if you have a floating-rate loan. When the repo rate or MCLR changes, your bank adjusts your interest rate. Banks typically handle this in one of two ways: they either change your EMI amount while keeping the tenure the same, or they keep your EMI the same and change the tenure. Most banks default to changing the tenure. You can ask your bank to switch to the EMI-change method if you prefer predictable timelines. During 2022-2023, many borrowers saw their tenures extend from 20 years to 25-28 years without realizing it because their EMI stayed the same while rates went up.

The Bottom Line

A home loan is probably the largest financial commitment you will make in your life. The difference between a well-planned home loan and a poorly planned one can be Rs 20-30 lakh over 20 years.

Here is your action checklist:

- Calculate your EMI using our Home Loan EMI Calculator before visiting any bank

- Cap your EMI at 30-35% of your take-home salary, not what the bank approves

- Budget for hidden costs (stamp duty, registration, processing fee) which add 8-12% to property value

- Choose a repo rate-linked loan for faster rate transmission

- Start prepaying from year 1, even Rs 5,000 extra per month saves lakhs

- Run the rent vs buy math for your specific city using our Rent vs Buy Calculator

If your CIBIL score is below 700 and you are worried about approval, read our guide on How to Get a Home Loan with Low CIBIL Score.

Browse all loan products and comparisons to find the best rates available right now.

Home Loan EMI Calculator

Calculate your monthly EMI

- Instant EMI for any loan amount & tenure

- See total interest vs principal breakup

- Compare prepayment savings scenarios