Every Indian resident whose gross total income exceeds ₹3 lakh under the new tax regime or ₹2.5 lakh under the old tax regime must file an Income Tax Return (ITR) with the Income Tax Department before July 31, 2026 for the financial year 2025-26 (Assessment Year 2026-27). An Income Tax Return is a prescribed form in which a taxpayer declares their total income, applicable deductions, exemptions, and tax liability for a given financial year. Filing ITR is not just a legal obligation — it serves as proof of income for visa applications, loan approvals, and government tenders. Even if your income falls below the taxable threshold, filing a return can help you claim TDS refunds, carry forward losses, and build a documented financial history.

The Income Tax Department has made the entire filing process digital through the e-filing portal at incometax.gov.in. Whether you are a salaried employee, freelancer, business owner, or investor, this guide walks you through every step of filing your ITR online for FY 2025-26 — from gathering documents to e-verification.

Key Takeaways

- Deadline: July 31, 2026 is the last date to file ITR for FY 2025-26 (AY 2026-27) without penalty for individuals and HUFs not subject to audit.

- Choose the right form: Most salaried individuals with income up to ₹50 lakh use ITR-1 (Sahaj). Business owners and professionals use ITR-3 or ITR-4.

- Documents needed: Form 16, Form 26AS, Annual Information Statement (AIS), bank statements, investment proofs under Section 80C/80D, and capital gains statements.

- New regime is default: The new tax regime (with no deductions but lower slab rates) is the default from FY 2023-24 onwards. You must explicitly opt out to use the old regime.

- e-Verification is mandatory: Your return is not treated as filed until you e-verify it within 30 days of submission using Aadhaar OTP, net banking, or Digital Signature Certificate (DSC).

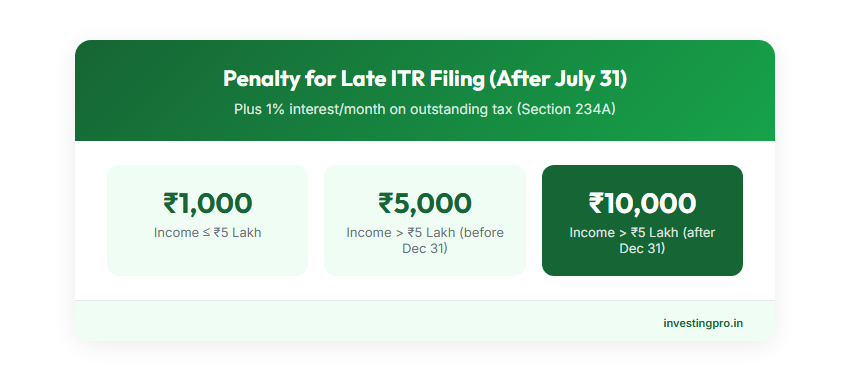

- Penalty for late filing: ₹5,000 if filed after July 31 but before December 31, 2026. ₹10,000 if filed after December 31. Reduced to ₹1,000 if total income is below ₹5 lakh.

Who Must File an Income Tax Return in India?

Filing ITR is mandatory if your gross total income (before deductions under Chapter VI-A) exceeds the basic exemption limit. The thresholds differ based on your chosen tax regime and age group.

Income Thresholds for Mandatory Filing

| Category | Old Regime (FY 2025-26) | New Regime (FY 2025-26) |

|---|---|---|

| Individuals below 60 years | ₹2.5 lakh | ₹3 lakh |

| Senior Citizens (60-79 years) | ₹3 lakh | ₹3 lakh |

| Super Senior Citizens (80+ years) | ₹5 lakh | ₹3 lakh |

| HUFs | ₹2.5 lakh | ₹3 lakh |

Mandatory Filing Even If Income Is Below Threshold

Regardless of your income level, you must file an ITR if any of these conditions apply:

- You want to claim a TDS or TCS refund — the only way to get your refund is by filing a return.

- You have deposited ₹1 crore or more in one or more current accounts during the financial year.

- You have spent ₹2 lakh or more on foreign travel during the year.

- You have incurred electricity expenditure exceeding ₹1 lakh during the year.

- Your total TDS/TCS deducted is ₹25,000 or more (₹50,000 for senior citizens).

- You hold any foreign assets, foreign income, or signing authority in a foreign account.

- Your business turnover exceeds ₹60 lakh or professional gross receipts exceed ₹10 lakh.

- You have deposited more than ₹50 lakh in savings accounts during the year.

- You want to carry forward losses (capital losses, business losses) to future years for set-off.

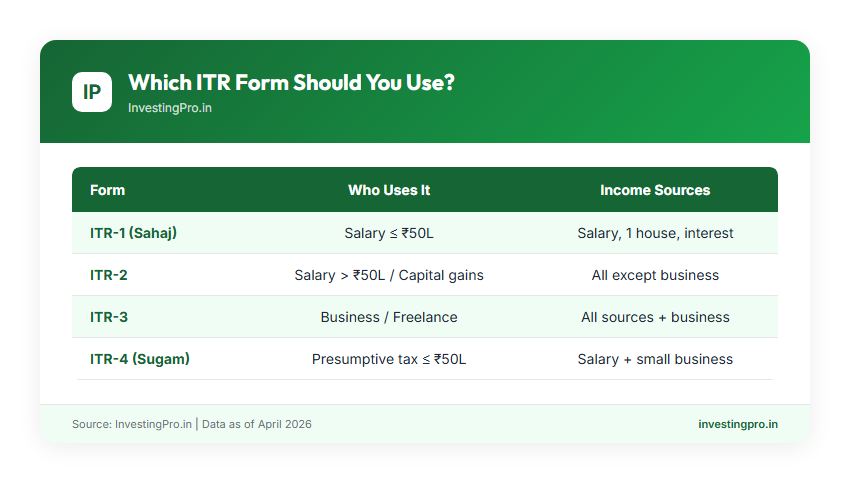

Which ITR Form Should You Use?

| ITR Form | Who Should Use | Income Sources Covered |

|---|---|---|

| ITR-1 (Sahaj) | Resident individuals with total income up to ₹50 lakh | Salary/Pension, One house property, Other sources (interest, dividends up to ₹5,000), Agricultural income up to ₹5,000 |

| ITR-2 | Individuals and HUFs with income above ₹50 lakh, capital gains, foreign assets, multiple house properties | All income sources except business/profession. Includes capital gains, foreign income, more than one house property |

| ITR-3 | Individuals and HUFs with business or professional income (not opting for presumptive taxation) | All income sources including business/profession income with full books of accounts |

| ITR-4 (Sugam) | Individuals, HUFs, and firms with total income up to ₹50 lakh opting for presumptive taxation | Salary/Pension, One house property, Other sources, Business income under presumptive scheme |

| ITR-5 | Partnership firms, LLPs, AOPs, BOIs, and cooperative societies | All income sources for entities that are not individuals, HUFs, or companies |

| ITR-6 | Companies other than those claiming exemption under Section 11 | All income sources for companies. Must be filed electronically |

| ITR-7 | Trusts, political parties, charitable institutions | Income of trusts, institutions, and associations with specific exemptions |

Quick guide: Salaried with income under ₹50 lakh and no capital gains — use ITR-1. Sold mutual funds, stocks, or property — use ITR-2. Freelance or business income — use ITR-3 or ITR-4.

Documents You Need Before Filing ITR

Identity and Basic Documents

- PAN Card — mandatory for filing. Must be linked with Aadhaar.

- Aadhaar Card — required for e-verification and PAN-Aadhaar linking.

- Bank account details — account number, IFSC code for refund. Pre-validate at least one bank account on the e-filing portal.

Income Documents

- Form 16 — from employer. Contains salary breakup, TDS deducted.

- Form 16A — TDS certificates for non-salary income (FD interest, rent TDS).

- Form 26AS — download from TRACES. Shows all TDS/TCS credited against your PAN.

- Annual Information Statement (AIS) — comprehensive financial data. Cross-check carefully.

- Bank statements — for savings/FD interest income.

- Capital gains statements — from your broker (Zerodha, Groww, Upstox) and CAMS/KFintech.

- Rental income details — rent received, municipal taxes paid, home loan interest certificate.

Deduction and Exemption Proofs

- Section 80C proofs — PPF passbook, ELSS statements, life insurance receipts, NSC, tuition fees, home loan principal. Read our Section 80C Complete Guide.

- Section 80D — health insurance premium receipts (self + parents).

- Section 80CCD(1B) — NPS contribution receipt. See NPS Tax Benefits Guide.

- Section 24(b) — home loan interest certificate from bank.

- Section 80E — education loan interest certificate.

- Section 80G — donation receipts.

- HRA proofs — rent receipts, landlord PAN (if rent > ₹1 lakh/year).

Important: Deductions under Chapter VI-A (80C, 80D, etc.) are not available under the new tax regime except Section 80CCD(2). Compare both regimes using our Old vs New Regime Calculator.

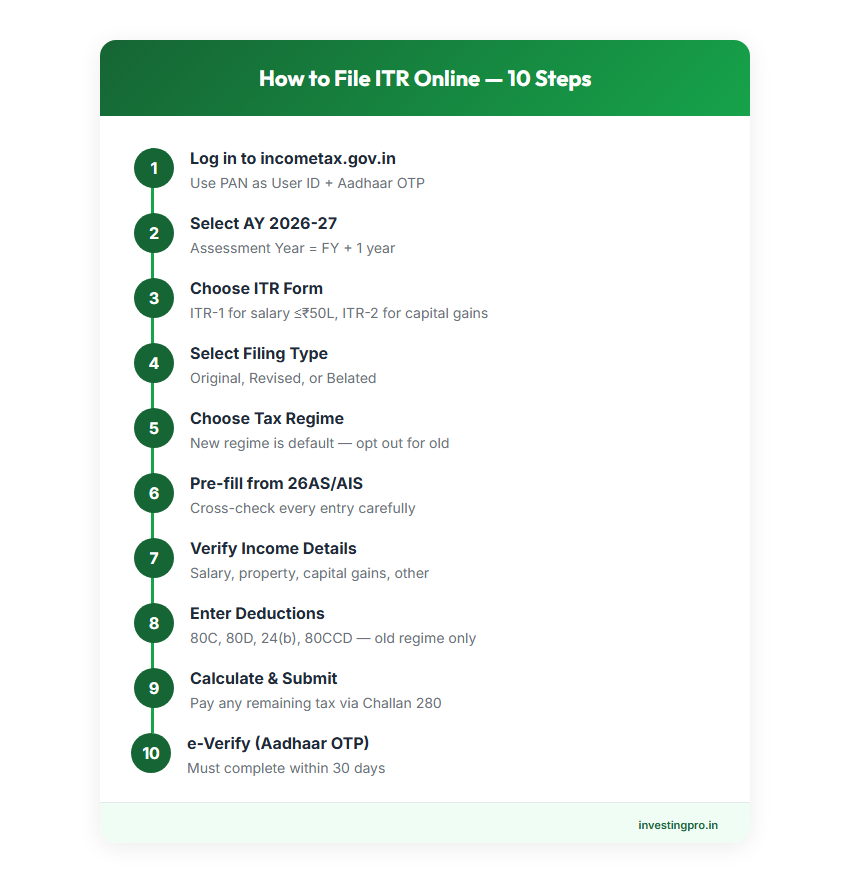

Step-by-Step: How to File ITR Online for FY 2025-26

Step 1: Log In to the e-Filing Portal

Visit incometax.gov.in and click "Login." Enter your PAN number as User ID, password, and OTP sent to your registered mobile. First-time filers: click "Register" to create an account using PAN, Aadhaar, and mobile number.

Navigate to e-File → Income Tax Returns → File Income Tax Return.

Step 2: Select Assessment Year (AY 2026-27)

Select Assessment Year 2026-27. The assessment year is always one year ahead of the financial year. Choose Online filing mode (recommended) or Offline (JSON utility).

Step 3: Choose Your ITR Form

The portal may suggest a form based on pre-filled data. Verify against the ITR form table above. Wrong form selection leads to a defective return notice under Section 139(9).

Step 4: Select Filing Type

- Original (Section 139(1)) — first-time filing for this AY.

- Revised (Section 139(5)) — correcting a previously filed return.

- Belated (Section 139(4)) — filing after July 31 but before December 31.

Step 5: Choose Your Tax Regime (Old vs New)

The new tax regime is the default from FY 2023-24. To use the old regime (allowing 80C, 80D, HRA deductions), file Form 10-IEA before filing your return.

| Income Slab | Old Regime Rate | New Regime Rate |

|---|---|---|

| Up to ₹2.5L (Old) / ₹3L (New) | Nil | Nil |

| ₹2.5-5L (Old) / ₹3-7L (New) | 5% | 5% |

| ₹5-10L (Old) / ₹7-10L (New) | 20% | 10% |

| ₹10-12L (New) | 30% | 15% |

| ₹12-15L (New) | 30% | 20% |

| Above ₹15L (New) / Above ₹10L (Old) | 30% | 30% |

Use our Income Tax Calculator to compare both regimes. Read: Old vs New Tax Regime — Which Is Better?

Step 6: Pre-fill Data from Form 26AS and AIS

Click "Pre-fill". The portal fetches income data automatically. Do not blindly accept pre-filled data. Cross-check every entry. Common mismatches: FD interest amounts, MF capital gains showing redemption instead of gains, missing dividend entries.

Step 7: Verify and Enter Income Details

Salary: Verify gross salary, HRA, standard deduction (₹75,000 new / ₹50,000 old), professional tax. Match with Form 16.

House Property: Self-occupied = nil value, claim home loan interest under Section 24(b). Let-out = annual rent minus municipal taxes minus 30% standard deduction.

Capital Gains: STCG on equity at 20%, LTCG on equity at 12.5% (above ₹1.25 lakh exemption). Import broker statements for accuracy.

Other Sources: Savings interest, FD interest, dividends, gifts above ₹50,000.

Step 8: Enter Deductions (Old Regime Only)

Key deductions: Section 80C (₹1.5 lakh), 80CCD(1B) (₹50,000 NPS), 80D (₹25K-₹1 lakh health insurance), Section 24(b) (₹2 lakh home loan interest), 80E (education loan interest), 80G (donations). See our complete 80C guide and salary tax saving guide.

Step 9: Calculate Tax, Review, and Submit

Click "Calculate Tax". The portal shows: no tax due, tax payable (pay via Challan 280), or refund due (ensure bank is pre-validated). Review every schedule before submitting.

Step 10: e-Verify Your Return

Your ITR is not valid until e-verified within 30 days. Three methods:

- Aadhaar OTP (recommended) — fastest, takes under 2 minutes.

- Net Banking — through pre-validated banks (SBI, ICICI, HDFC).

- Digital Signature Certificate (DSC) — for companies and professionals.

After verification, save the ITR-V acknowledgment — it is your proof of filing.

Tax Calculation Examples for FY 2025-26

Example 1: ₹7.5 Lakh Salaried (Zero Tax Under New Regime)

| Particulars | New Regime | Old Regime |

|---|---|---|

| Gross Salary | ₹7,50,000 | ₹7,50,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| 80C + 80D | Not allowed | ₹1,75,000 |

| Net Taxable Income | ₹6,75,000 | ₹5,25,000 |

| Tax Before Rebate | ₹18,750 | ₹15,000 |

| Section 87A Rebate | ₹18,750 (full) | ₹12,500 |

| Tax Payable | ₹0 | ₹2,600 |

Verdict: New regime gives zero tax at ₹7.5 lakh.

Example 2: ₹12 Lakh Salaried (Old vs New Comparison)

| Particulars | New Regime | Old Regime |

|---|---|---|

| Gross Salary | ₹12,00,000 | ₹12,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| HRA Exemption | Not allowed | ₹1,80,000 |

| 80C + 80D + NPS | Not allowed | ₹2,50,000 |

| Net Taxable Income | ₹11,25,000 | ₹7,20,000 |

| Total Tax | ₹74,100 | ₹46,176 |

Verdict: With substantial deductions, old regime saves ₹28,000 at ₹12 lakh salary.

Example 3: ₹20 Lakh with Capital Gains + Rental Income

| Income Source | Amount |

|---|---|

| Salary (gross) | ₹15,00,000 |

| Rental Income | ₹3,60,000 |

| STCG (equity) | ₹80,000 |

| LTCG (equity, above exemption) | ₹60,000 |

| Total Tax (New Regime) | ₹2,04,464 |

Capital gains are taxed at special rates regardless of regime. This taxpayer must file ITR-2.

Common Mistakes to Avoid

1. Not Reconciling Form 26AS/AIS

The department auto-checks declared income against 26AS/AIS. Mismatches trigger notices. Always reconcile before filing.

2. Forgetting Bank Interest and FD Income

Interest from all accounts is taxable and tracked via AIS. Not declaring it is the fastest way to get a notice.

3. Choosing the Wrong ITR Form

Sold mutual funds but filed ITR-1? That's a defective return. Verify form eligibility first.

4. Not e-Verifying Within 30 Days

Without e-verification, your return is treated as never filed. Verify immediately with Aadhaar OTP.

5. Ignoring Capital Gains from MF Redemptions

Every redemption, SWP, and switch is taxable. Download consolidated statement from CAMS/KFintech.

6. Not Claiming TDS Refund

If TDS exceeds actual tax liability, file ITR to claim the refund. Many leave lakhs unclaimed.

7. Filing After Deadline Without Understanding Penalties

Late filing = no loss carry forward + penalties + higher future TDS. Pay self-assessed tax by July 31 at minimum.

Penalties for Late Filing

| Total Income | After July 31 (before Dec 31) | After December 31 |

|---|---|---|

| Up to ₹5 lakh | ₹1,000 | ₹1,000 |

| Above ₹5 lakh | ₹5,000 | ₹10,000 |

Additional: 1% interest per month on outstanding tax (Section 234A), loss of carry forward rights, higher future TDS under Section 206AB.

When to File a Revised Return

Mistakes in your original ITR? File a revised return under Section 139(5) before December 31, 2026. No penalty for revision. Reasons: missed income, wrong deduction, wrong form, regime switch (salary-only taxpayers), or revised Form 16 from employer.

Frequently Asked Questions

What is the last date to file ITR for FY 2025-26?

July 31, 2026 for individuals and HUFs not requiring audit. October 31, 2026 for businesses requiring audit. November 30, 2026 for transfer pricing cases.

Can I file ITR without Form 16?

Yes. Use salary slips and download Form 26AS + AIS from the e-filing portal to verify TDS details. Form 16 is a TDS certificate — the data is already in 26AS.

Which regime should I choose — old or new?

New regime if total deductions are below ~₹3.75 lakh. Old regime if deductions exceed that. Use our Tax Calculator to compare exact numbers for your salary.

Do I need a CA to file ITR?

Not for most salaried individuals. The portal's guided process handles ITR-1 and ITR-2 well. Consider a CA for complex business income, foreign assets, or department notices. Fees: ₹1,000-₹3,000 for salary returns.

What is e-verification and how to do it?

Digital signature for your return. Fastest method: Aadhaar OTP — enter OTP sent to Aadhaar-linked mobile. Alternatives: net banking or DSC. Must complete within 30 days of filing.

Can I switch regime after filing?

Salary-only taxpayers: yes, by filing revised return before December 31. Business income: more restrictive — one-time switch from new to old requires Form 10-IEA before July 31 due date.

What if I have income from multiple sources?

Use the correct ITR form: salary + capital gains = ITR-2, salary + business = ITR-3. Report all sources — the department cross-references AIS data across all PANs and bank accounts.

Is ITR filing mandatory if income is below taxable limit?

Not legally mandatory (unless mandatory filing conditions apply). But strongly recommended for TDS refunds, loss carry forward, loan applications, and visa documentation.

How to claim TDS refund?

File ITR with correct income. If TDS (from 26AS) exceeds your tax liability, the excess is auto-refunded to your pre-validated bank account within 30-60 days with interest under Section 244A.

What happens if I don't file ITR?

Penalty up to ₹10,000, loss of carry forward rights, double TDS on future income under Section 206AB, risk of prosecution for tax dues above ₹10,000, and best judgment assessment under Section 144.

Disclaimer: This article is for educational purposes and is based on the Income Tax Act provisions applicable for FY 2025-26 (AY 2026-27). Tax laws are subject to change. The calculations shown are illustrative. Always verify current rules on incometax.gov.in and consult a qualified Chartered Accountant before making financial decisions. InvestingPro.in does not provide tax filing services or personalised tax advice.