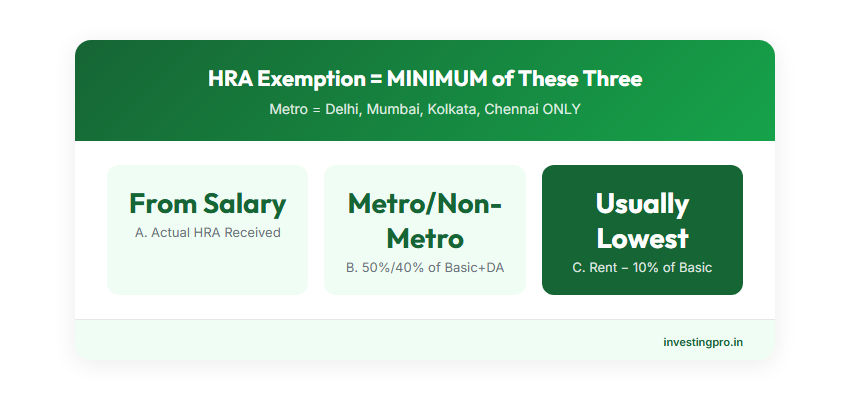

House Rent Allowance (HRA) exemption under Section 10(13A) of the Income Tax Act allows salaried employees in India to claim tax deductions on rent paid. The exemption is calculated as the minimum of three amounts: actual HRA received, 50% of basic salary (metro) or 40% (non-metro), and rent paid minus 10% of basic salary. For the financial year 2025-26 (assessment year 2026-27), HRA remains one of the most significant tax-saving tools available to salaried individuals under the old tax regime. If you are paying rent and your salary includes an HRA component, understanding this calculation can save you anywhere from ₹15,000 to ₹2 lakh or more in taxes every year.

Despite being one of the oldest tax exemptions in India, HRA is widely misunderstood. Many employees either fail to claim it properly, overclaim it and face scrutiny, or don't know they can claim it even when paying rent to parents. This guide breaks down every aspect of HRA exemption — the formula, worked examples with real numbers, metro vs non-metro rules, documentation requirements, and common mistakes that trigger income tax notices.

Key Takeaways

- HRA exemption is the lowest of three amounts — actual HRA received, 50%/40% of basic salary, or rent paid minus 10% of basic salary. You don't get to choose — the Income Tax Act mandates the minimum.

- Metro cities get a higher exemption — 50% of (Basic + DA) for Delhi, Mumbai, Kolkata, and Chennai. All other cities use 40%. This single distinction can change your exemption by ₹20,000–₹60,000 annually.

- Paying rent to parents is fully legal — your parents must declare the rental income in their ITR, and you need proper rent receipts. If total rent exceeds ₹1 lakh per year, your parent's PAN is mandatory.

- HRA is NOT available under the new tax regime — if you opted for the new regime (default from FY 2023-24), you cannot claim HRA exemption. Switch back to the old regime if HRA savings exceed the new regime's lower rates.

- No upper limit on HRA exemption — unlike Section 80C (capped at ₹1.5 lakh), HRA exemption has no absolute cap. It is limited only by the formula. High-rent, high-salary individuals can claim ₹3–5 lakh or more.

- Landlord PAN is required if rent exceeds ₹1 lakh/year — failing to provide this is the single most common reason for HRA claims being rejected during assessment.

HRA Exemption Formula — The 3-Component Rule

The HRA exemption under Section 10(13A) read with Rule 2A of the Income Tax Rules is calculated as the minimum (lowest) of the following three amounts:

| Component | Formula | Notes |

|---|---|---|

| A — Actual HRA Received | HRA component from salary slip | As per employer's salary structure |

| B — 50% or 40% of Salary | 50% × (Basic + DA) for metro cities40% × (Basic + DA) for non-metro cities | Metro = Delhi, Mumbai, Kolkata, Chennai only |

| C — Rent Minus 10% of Salary | Annual Rent Paid − 10% × (Basic + DA) | If result is negative, exemption is zero |

HRA Exemption = Minimum of (A, B, C)

A few important clarifications on the formula:

- Salary means Basic + Dearness Allowance (DA) — not your gross salary or CTC. Special allowances, bonuses, and other components are excluded.

- DA is included only if it forms part of retirement benefits — in government jobs, DA is always included. In private sector, check if your DA counts towards PF/gratuity.

- The calculation is done on a monthly basis — if your rent, salary, or city changed during the year, calculate each month separately and add them up.

5 Worked Examples with Full Calculations

Example 1: ₹8 Lakh Salary, ₹15,000 Rent, Delhi (Metro)

| Particulars | Monthly (₹) | Annual (₹) |

|---|---|---|

| Basic Salary | 33,333 | 4,00,000 |

| DA (assumed nil) | 0 | 0 |

| HRA Received | 16,667 | 2,00,000 |

| Rent Paid | 15,000 | 1,80,000 |

Calculation (annual):

- A — Actual HRA received: ₹2,00,000

- B — 50% of (Basic + DA): 50% × ₹4,00,000 = ₹2,00,000 (Delhi is metro)

- C — Rent paid minus 10% of (Basic + DA): ₹1,80,000 − (10% × ₹4,00,000) = ₹1,80,000 − ₹40,000 = ₹1,40,000

HRA Exemption = Minimum of (₹2,00,000, ₹2,00,000, ₹1,40,000) = ₹1,40,000

At the 20% tax slab (income ₹5–10 lakh under old regime), this saves approximately ₹28,000 + 4% cess = ₹29,120 in tax.

Example 2: ₹12 Lakh Salary, ₹20,000 Rent, Bengaluru (Metro)

| Particulars | Monthly (₹) | Annual (₹) |

|---|---|---|

| Basic Salary | 50,000 | 6,00,000 |

| DA | 0 | 0 |

| HRA Received | 25,000 | 3,00,000 |

| Rent Paid | 20,000 | 2,40,000 |

Calculation (annual):

- A — Actual HRA received: ₹3,00,000

- B — 50% of (Basic + DA): 50% × ₹6,00,000 = ₹3,00,000 (Bengaluru is metro)

- C — Rent paid minus 10% of (Basic + DA): ₹2,40,000 − ₹60,000 = ₹1,80,000

HRA Exemption = Minimum of (₹3,00,000, ₹3,00,000, ₹1,80,000) = ₹1,80,000

At the 30% tax slab (income above ₹10 lakh under old regime), tax saved = 30% × ₹1,80,000 = ₹54,000 + 4% cess = ₹56,160. This is significant — nearly five months of rent recovered through tax savings alone.

Example 3: ₹6 Lakh Salary, ₹10,000 Rent, Jaipur (Non-Metro)

| Particulars | Monthly (₹) | Annual (₹) |

|---|---|---|

| Basic Salary | 25,000 | 3,00,000 |

| DA | 0 | 0 |

| HRA Received | 10,000 | 1,20,000 |

| Rent Paid | 10,000 | 1,20,000 |

Calculation (annual):

- A — Actual HRA received: ₹1,20,000

- B — 40% of (Basic + DA): 40% × ₹3,00,000 = ₹1,20,000 (Jaipur is non-metro)

- C — Rent paid minus 10% of (Basic + DA): ₹1,20,000 − ₹30,000 = ₹90,000

HRA Exemption = Minimum of (₹1,20,000, ₹1,20,000, ₹90,000) = ₹90,000

At the 20% slab, tax saved = 20% × ₹90,000 = ₹18,000 + cess = ₹18,720. Notice how the non-metro 40% rate still doesn't affect this case — Component C (rent minus 10%) is the limiting factor, as it usually is.

Example 4: ₹18 Lakh Salary, ₹35,000 Rent, Mumbai (Metro)

| Particulars | Monthly (₹) | Annual (₹) |

|---|---|---|

| Basic Salary | 75,000 | 9,00,000 |

| DA | 0 | 0 |

| HRA Received | 37,500 | 4,50,000 |

| Rent Paid | 35,000 | 4,20,000 |

Calculation (annual):

- A — Actual HRA received: ₹4,50,000

- B — 50% of (Basic + DA): 50% × ₹9,00,000 = ₹4,50,000

- C — Rent paid minus 10% of (Basic + DA): ₹4,20,000 − ₹90,000 = ₹3,30,000

HRA Exemption = Minimum of (₹4,50,000, ₹4,50,000, ₹3,30,000) = ₹3,30,000

At the 30% slab, tax saved = 30% × ₹3,30,000 = ₹99,000 + cess = ₹1,02,960. For high-rent Mumbai professionals, HRA alone can save over ₹1 lakh in taxes. This is why salary restructuring to maximize basic pay (and thereby HRA) is so valuable.

Example 5: ₹10 Lakh Salary, Pays Rent to Parents

| Particulars | Monthly (₹) | Annual (₹) |

|---|---|---|

| Basic Salary | 41,667 | 5,00,000 |

| DA | 0 | 0 |

| HRA Received | 20,833 | 2,50,000 |

| Rent Paid to Father | 15,000 | 1,80,000 |

Calculation (annual):

- A — Actual HRA received: ₹2,50,000

- B — 50% of (Basic + DA): 50% × ₹5,00,000 = ₹2,50,000 (assuming metro)

- C — Rent paid minus 10% of (Basic + DA): ₹1,80,000 − ₹50,000 = ₹1,30,000

HRA Exemption = Minimum of (₹2,50,000, ₹2,50,000, ₹1,30,000) = ₹1,30,000

At the 20% slab, tax saved = ₹27,040 (including cess). The father must declare ₹1,80,000 as rental income in his ITR. If the father is a senior citizen with income below the basic exemption limit (₹3 lakh), he pays zero tax on this rental income. The family nets ₹27,040 in tax savings. Since total rent is ₹1,80,000/year (above ₹1 lakh), the father's PAN must be furnished to the employer.

Metro vs Non-Metro Cities — The 50% vs 40% Rule

The Income Tax Act defines only four cities as metro for HRA purposes:

| Metro Cities (50% of Basic + DA) | Non-Metro Cities (40% of Basic + DA) |

|---|---|

| Delhi (including NCR for some employers) | Bengaluru |

| Mumbai (including Navi Mumbai, Thane) | Hyderabad |

| Kolkata | Pune |

| Chennai | Ahmedabad |

| Jaipur, Lucknow, Chandigarh, and all other cities |

Important clarification: Many people assume Bengaluru, Hyderabad, and Pune are metro cities for HRA. They are not. The IT Act's definition has not been updated since its inception and only includes the original four metros. This means a person earning ₹10 lakh in Bengaluru gets 40% (₹2,00,000), while the same person in Chennai gets 50% (₹2,50,000) — a difference of ₹50,000 in the exemption calculation.

However, in practice, Component C (rent minus 10% of salary) is usually the limiting factor for most people. The metro/non-metro distinction matters most when your rent is very high relative to your salary, pushing Component C above Component B.

If you move cities mid-year: Calculate HRA month by month. For the months you lived in a metro city, use 50%. For months in a non-metro city, use 40%. Add up all 12 months for your annual exemption.

HRA When Paying Rent to Parents

Paying rent to parents and claiming HRA exemption is completely legal and well-established in Indian tax law. The Income Tax Appellate Tribunal (ITAT) has upheld this arrangement in multiple cases. Here is how to structure it correctly:

Conditions for Claiming HRA on Rent Paid to Parents

- You must actually pay the rent — transfer money via bank (NEFT/UPI/cheque). Cash payments are valid but harder to prove. Maintain a clear paper trail.

- The house must be owned by the parent — you cannot pay rent to a parent who doesn't own the house. If the house is in your mother's name, pay rent to her.

- You must not be an owner of the property — if the house is jointly owned by you and your parent, you cannot claim HRA for the portion you own.

- Rent receipts are mandatory — get proper rent receipts signed by your parent every month (or quarterly). Include the parent's name, address of the property, period, and amount.

- Parent's PAN is required if rent exceeds ₹1 lakh/year — furnish this to your employer during proof submission.

- Parent must declare rental income — the parent must show this as "Income from House Property" in their ITR. They can claim 30% standard deduction on this rental income under Section 24.

Why This Works as a Tax-Saving Strategy

Consider a family where the son earns ₹15 lakh (30% slab) and the retired father has pension income of ₹4 lakh (5% slab under old regime). The son pays ₹18,000/month rent to the father.

- Son's tax saving: HRA exemption of approximately ₹1.5 lakh → saves ₹46,800 (30% + cess)

- Father's additional tax: Rental income ₹2,16,000 minus 30% standard deduction = ₹1,51,200 taxable. At 5% slab = ₹7,560 tax

- Net family saving: ₹46,800 − ₹7,560 = ₹39,240 per year

If the parent's total income (including the rent) stays below ₹3 lakh (senior citizen) or ₹5 lakh (with rebate under Section 87A), the family saves the entire ₹46,800 with zero additional tax.

Rent Agreement with Parents

While not strictly mandatory, having a formal rent agreement with your parents strengthens your claim significantly. Draft a simple agreement on stamp paper (₹100-500 depending on state) mentioning:

- Names of tenant (you) and landlord (parent)

- Address of the rented property

- Monthly rent amount and payment mode

- Duration of the agreement

- Signatures of both parties

HRA When You Own a Home

This is one of the most asked questions in Indian tax planning: Can you claim HRA exemption if you own a house? The answer is yes — with conditions.

Scenario 1: Own a House in a Different City

If you own a house in Jaipur but work and live on rent in Mumbai, you can claim:

- HRA exemption — for rent paid in Mumbai

- Home loan interest deduction — under Section 24 (up to ₹2 lakh for self-occupied, or full interest for let-out property)

- Home loan principal deduction — under Section 80C (up to ₹1.5 lakh)

This is the most straightforward case. There is no conflict because the properties are in different cities. The Jaipur house is treated as self-occupied (or let-out if rented), and HRA applies to your Mumbai rental.

Scenario 2: Own a House in the Same City

This is where it gets tricky. If you own a house in Mumbai and also rent another place in Mumbai, the tax department may question why you are not living in your own house. However, there are legitimate reasons:

- Your own house is too far from your workplace

- Your own house is let out to tenants

- Your own house is under renovation

If you can demonstrate a genuine reason for renting separately, the claim is valid. But expect scrutiny. Keep documentation of why you cannot live in your own house. If your own house is let out, report the rental income and you can still claim HRA on the house you live in.

Scenario 3: Home Loan EMI but No HRA Component

If your employer doesn't give you HRA but you pay rent, look at Section 80GG (covered below). You cannot claim HRA exemption under Section 10(13A) without an HRA component in your salary.

For a detailed comparison of all deductions available, use our Income Tax Calculator to see your exact savings under both old and new regimes.

Documents Required for HRA Claim

When submitting investment proofs to your employer (usually in January-February), you need the following documents for HRA:

| Document | When Required | Details |

|---|---|---|

| Rent Receipts | Always | Monthly or quarterly receipts signed by the landlord. Must include landlord name, address, tenant name, period, amount, and revenue stamp (₹1) if payment is in cash. |

| Rent Agreement | Strongly recommended | Formal agreement on stamp paper. Many employers mandate this. Essential if paying rent to parents or relatives. |

| Landlord PAN | If rent > ₹1,00,000/year | Mandatory under Rule 2A. Without this, employer must deduct tax on the full HRA amount. Self-declaration by landlord is not sufficient. |

| Declaration Form | As per employer policy | Employer-specific form declaring rent paid, landlord details, and property address. Some companies use Form 12BB. |

| Bank Statements | If questioned | Proof of rent payments via bank transfer. Keeps your claim airtight during assessment proceedings. |

Rent Receipt Format

A valid rent receipt must contain:

- Date of payment

- Tenant's name (your name)

- Landlord's name and signature

- Address of the rented property

- Amount paid (in figures and words)

- Period covered (e.g., "For the month of April 2025")

- Revenue stamp of ₹1 if paid in cash (not needed for bank transfers)

Pro tip: Even if you pay rent via UPI or bank transfer, still collect rent receipts. Bank statements prove the payment, but rent receipts prove the purpose. Many employers insist on both.

HRA Under the New Tax Regime — Not Available

This is the single most important thing to know: HRA exemption under Section 10(13A) is NOT available under the new tax regime. If you have opted for the new regime (which is the default from FY 2023-24 onwards), your entire HRA is taxable as part of salary income.

| Feature | Old Tax Regime | New Tax Regime (Default) |

|---|---|---|

| HRA Exemption (Section 10(13A)) | Available | NOT Available |

| Standard Deduction | ₹50,000 | ₹75,000 |

| Section 80C (₹1.5 lakh) | Available | NOT Available |

| Section 80D (Health Insurance) | Available | NOT Available |

| Home Loan Interest (Section 24) | Up to ₹2 lakh | NOT Available (self-occupied) |

| Section 80GG (Rent without HRA) | Available | NOT Available |

When Should You Choose the Old Regime for HRA?

The old regime is better when your total deductions and exemptions (HRA + 80C + 80D + home loan interest + NPS + others) exceed the tax savings from the new regime's lower slab rates. As a rough rule:

- Salary up to ₹8 lakh: New regime is usually better (rebate under Section 87A makes tax nil up to ₹7 lakh)

- Salary ₹8-15 lakh with rent: Old regime is often better, especially in metros with high rent

- Salary above ₹15 lakh with heavy deductions: Old regime almost always wins if you have HRA + 80C + 80D + home loan

Use our Old vs New Tax Regime Calculator to compare both regimes with your exact salary and deductions. The difference can be ₹50,000 or more for high-rent professionals.

Section 80GG — For Those Without HRA

If you are self-employed, a freelancer, or your employer does not provide an HRA component in your salary, you can still claim a deduction for rent paid under Section 80GG.

Conditions for Claiming Section 80GG

- You are self-employed OR your salary does not include HRA

- You, your spouse, or your minor child do not own a residential property in the city where you work

- You do not own a residential property at any other location for which you are claiming self-occupied property benefits

- You have filed Form 10BA — a declaration that you are paying rent and not receiving HRA

Section 80GG Deduction Amount

The deduction under 80GG is the minimum of:

| Component | Formula |

|---|---|

| A — Fixed limit | ₹5,000 per month (₹60,000 per year) |

| B — Percentage of income | 25% of total income (after all other deductions) |

| C — Rent minus 10% | Rent paid minus 10% of total income |

The maximum deduction is effectively capped at ₹60,000 per year (₹5,000/month), which is significantly lower than HRA exemption. This is why salaried individuals should always negotiate for HRA in their salary structure rather than relying on 80GG.

For example, a freelancer earning ₹8 lakh annually and paying ₹12,000/month rent:

- A: ₹60,000

- B: 25% × ₹8,00,000 = ₹2,00,000

- C: ₹1,44,000 − ₹80,000 = ₹64,000

- Deduction = ₹60,000 (minimum of three, capped by Component A)

Common Mistakes That Can Cost You

1. Claiming HRA Under the New Tax Regime

Many employees submit rent receipts and claim HRA without realising they are on the new regime by default. Since FY 2023-24, the new regime is the default. You must actively opt for the old regime to claim HRA. Check with your employer during the financial year — some employers ask for regime choice at the start of the year. If you file ITR yourself, you can switch regimes when filing (for salaried individuals, you can switch every year).

2. Not Collecting Landlord PAN for Rent Above ₹1 Lakh/Year

If your annual rent exceeds ₹1 lakh (i.e., more than ₹8,333 per month), your employer is required to collect the landlord's PAN. If you fail to provide it, the employer must tax the full HRA as part of your salary. Many employees discover this in January when submitting proofs, and by then it may be too late to get the PAN from their landlord.

3. Fake Rent Receipts or Inflated Rent

The tax department has become increasingly sophisticated in detecting fake HRA claims. They cross-reference landlord PAN details, check if the landlord has declared the rental income, and verify property ownership. Penalties for fraudulent claims include 100%-300% of the tax evaded, plus potential prosecution under Section 276C. It is never worth the risk.

4. Not Calculating Month by Month When Details Change

If you moved cities in August (say from Pune to Mumbai), your HRA must be calculated separately for April-July (non-metro, 40%) and August-March (metro, 50%). Similarly, if your rent or salary changed mid-year, each period needs its own calculation. Many people use annual figures and apply a single percentage, which leads to either underclaiming or overclaiming.

5. Paying Rent to Spouse

Unlike paying rent to parents, paying rent to your spouse is not accepted for HRA exemption. The tax department considers husband and wife as a single economic unit for this purpose. This has been upheld in multiple ITAT decisions. If you are paying rent to live in a house owned by your spouse, you cannot claim HRA on it.

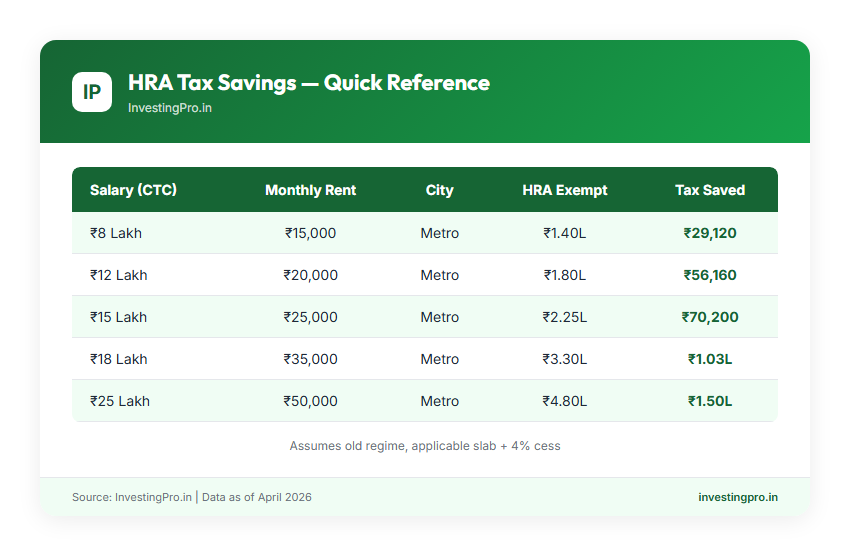

HRA Tax Exemption — Quick Reference Table

| Annual Salary (CTC) | Monthly Rent | City Type | Approx. HRA Exemption | Approx. Tax Saved |

|---|---|---|---|---|

| ₹5,00,000 | ₹8,000 | Non-Metro | ₹66,000 | ₹13,700 |

| ₹8,00,000 | ₹15,000 | Metro | ₹1,40,000 | ₹29,120 |

| ₹10,00,000 | ₹18,000 | Metro | ₹1,66,000 | ₹51,688 |

| ₹12,00,000 | ₹20,000 | Metro | ₹1,80,000 | ₹56,160 |

| ₹15,00,000 | ₹25,000 | Metro | ₹2,25,000 | ₹70,200 |

| ₹18,00,000 | ₹35,000 | Metro | ₹3,30,000 | ₹1,02,960 |

| ₹25,00,000 | ₹50,000 | Metro | ₹4,80,000 | ₹1,49,760 |

Note: Tax saved assumes old tax regime, applicable slab rate + 4% health and education cess. Actual amounts depend on your specific salary structure and other deductions. Use our Income Tax Calculator for exact figures.

Frequently Asked Questions

Can I claim HRA if I live in my own house?

If you live in your own house and do not pay rent to anyone, you cannot claim HRA exemption. The exemption specifically requires that you pay rent for a residential accommodation. However, if you own a house in one city and pay rent in another city where you work, you can claim HRA for the rented accommodation while also claiming home loan benefits on the owned property. See our guide on how to save tax on salary income for more strategies.

Is rent receipt mandatory for HRA claim?

Yes, rent receipts are required for claiming HRA exemption. Technically, if your annual rent is below ₹1 lakh, some employers may accept a self-declaration. But to be safe during income tax assessment, always maintain proper rent receipts regardless of the amount. Digital rent receipts (PDF with digital signature) are also accepted. If you pay via bank transfer, keep bank statements as additional proof, but they do not replace rent receipts.

Can I pay rent to my parents for HRA?

Yes, paying rent to parents is a legitimate and well-established tax-saving strategy. The Income Tax Appellate Tribunal (ITAT) has upheld this in numerous cases. Your parent must own the property, you must actually transfer the rent amount, your parent must declare the rental income in their ITR, and you must have proper rent receipts. If the annual rent exceeds ₹1 lakh, your parent's PAN is mandatory. This is especially effective when the parent is a senior citizen with income below the basic exemption limit, as the family achieves a net tax saving.

What if rent exceeds ₹1 lakh and landlord has no PAN?

If your landlord does not have a PAN and your annual rent exceeds ₹1 lakh, you have two options. First, request your landlord to apply for PAN — it takes about 15-20 days and can be done online. Second, if the landlord refuses, you can obtain a declaration from the landlord along with their name and address details. However, your employer may still deny the HRA exemption during salary processing. In that case, claim the exemption when filing your ITR directly. The employer's denial does not prevent you from claiming it at the ITR stage, provided you have all other documentation in order.

Is HRA available in the new tax regime?

No. HRA exemption under Section 10(13A) is not available under the new tax regime. If you choose the new regime (which is the default since FY 2023-24), your entire HRA becomes taxable. This also applies to Section 80GG for those without HRA. The new regime offers lower tax slab rates instead of exemptions and deductions. For employees paying significant rent, the old regime with HRA exemption often results in lower tax. Compare both using our Old vs New Regime Calculator.

Can I claim both HRA and home loan benefits?

Yes, you can claim both simultaneously if you own a home in one city and rent in another. For example, if you own a flat in Pune (paying EMI) and rent an apartment in Mumbai (where you work), you can claim: HRA exemption on Mumbai rent, home loan principal under Section 80C (up to ₹1.5 lakh), and home loan interest under Section 24 (up to ₹2 lakh for self-occupied, or full interest if the Pune property is let out). If both properties are in the same city, the claim is technically valid but may face scrutiny — maintain clear documentation of why you cannot live in your own house.

How to claim HRA if my employer doesn't provide it?

If your salary structure does not include an HRA component, you cannot claim exemption under Section 10(13A). Instead, claim a deduction under Section 80GG when filing your ITR. The maximum deduction under 80GG is ₹5,000 per month (₹60,000 per year). You must file Form 10BA along with your return. Additionally, you should consider asking your employer to restructure your salary to include HRA — most employers will do this at no additional cost since it doesn't change your CTC, only the components within it.

What is the maximum HRA exemption I can claim?

There is no absolute upper limit on HRA exemption. Unlike Section 80C which is capped at ₹1.5 lakh, HRA exemption is limited only by the formula — the minimum of (actual HRA received, 50%/40% of Basic + DA, rent paid minus 10% of Basic + DA). In practice, the exemption is most commonly limited by Component C (rent minus 10% of salary). For a person with ₹25 lakh salary and ₹50,000 monthly rent in Mumbai, the exemption can exceed ₹4.5 lakh. The key to maximising HRA is to ensure your basic salary is a high proportion of your CTC, as both HRA allocation and the formula use basic salary as the base.

How to Maximise Your HRA Tax Benefit

Beyond understanding the formula, here are actionable strategies to get the most out of HRA:

- Restructure your salary: Request your employer to allocate a higher percentage to basic salary. Since HRA is typically 40-50% of basic, a higher basic means higher HRA, which means a higher exemption ceiling. Many companies allow salary restructuring at the start of each financial year.

- Pay rent to parents if living at home: As covered above, this converts dead money (living at home for free) into a legitimate tax deduction. Structure it properly with rent receipts, bank transfers, and ensure your parent files their ITR.

- Keep all documentation from day one: Do not scramble in January when your employer asks for proofs. Set up a system — monthly rent receipts, rent agreement renewed annually, landlord PAN on file.

- Choose the right tax regime: If your HRA exemption is significant (above ₹1 lakh), the old regime is almost certainly better for you. Run the numbers through a tax calculator before choosing.

- Report accurately: Overclaiming HRA is one of the most common triggers for income tax notices. The department's computer system automatically flags cases where claimed HRA doesn't match TDS filings or where landlord PAN data doesn't match. Claim only what you are entitled to.

Disclaimer: This article is for informational and educational purposes only and does not constitute tax advice, legal advice, or financial advice. Tax laws and rates mentioned are based on the Income Tax Act, 1961 as applicable for FY 2025-26 (AY 2026-27) and are subject to change through Finance Act amendments or CBDT notifications. The examples and calculations are illustrative and may not reflect your exact tax situation. Always consult a qualified Chartered Accountant or tax professional before making tax-related decisions. InvestingPro.in and its authors are not responsible for any tax liability, penalty, or loss arising from the use of information in this article.